Critical minerals and policy reforms drive sustained growth in Asia Pacific’s mines

Asia Pacific is one of the world’s leading mining regions, endowed with abundant reserves, strong domestic demand and expanding downstream processing demand. According to the US Geological Survey, Asia Pacific accounted for 56.6% of total rare earths reserves in 2025, 42.3% of nickel reserves, and significant shares of reserves of lead (22.9%), zinc (20%), manganese (16.5%), iron ore (12.8%), silver (10.9%), gold (10.5%) and lithium (10%).

Major mining hubs within the Asia Pacific include China, India, Indonesia and the Philippines, and each faces its unique set of challenges. Despite its resource wealth, the industry is currently navigating a complex landscape shaped by existing internal challenges, including infrastructure gaps, high operational costs and policy instability, further intensified by external geopolitical pressures.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Meanwhile, Donald Trump’s tariffs and trade policies have created significant market volatility and geopolitical manoeuvring for the region’s mining industry. The US push to reduce reliance on Chinese supply chains is creating both disruptions and opportunities. For instance, on October 27, 2025, the US President Donald Trump signed agreements with Japan, Malaysia and Thailand to strengthen critical minerals cooperation and promote industry partnerships. This move by the US is to strengthen its supply chains apart from China. On the other hand, some APAC nations have deepened their own regional cooperation and trade ties with China to counteract the US pressure. Overall, countries are repositioning their strategic presence in the region with the current dynamics of trade and supply chain wars.

Coal remains the cornerstone of the Asia Pacific’s mining landscape, with the region accounting for 72.7% of global production in 2024. China stands out as the dominant producer, accounting for 71.3% of the region’s total output in 2024, while India and Indonesia contributed 16.3% and 12.5% shares, respectively. During the forecast period (2025-2030), coal production inthe Asia Pacific is projected to experience marginal growth, with a CAGR of 0.8%. This modest increase reflects a balanced scenario where anticipated supply decreases from Indonesia and China are expected to be largely offset by the robust supply growth from India, resulting in an overall subdued regional expansion. However, China will maintain its position as the region’s dominant producer throughout the outlook period, with an estimated 68.6% contribution in the region by 2030.

China’s coal mine output is expected to decline marginally over the forecast period, with a negative CAGR of 0.1%, due to competition from renewable sources, as well as issues with China’s lower-quality coal reserves, which will likely raise production costs. Key players operating in the Asia Pacific’s coal sector include CHN ENERGY Investment Group, China National Coal Group, Shaanxi Coal and Chemical Industry Group and Zijin Mining Group.

China remains a mining powerhouse, producing 51.8% of global coal, 43.2% of global lead, 33.7% of global zinc, 19.5% of global bauxite, 17.7% of global lithium and a notable share of 12.7% of global silver, 11.3% of global iron ore, 10.4% of global gold, and 9.8% of global manganese in 2024. Overall, China’s extensive domestic reserves, significant state investment, large-scale production of various minerals and its presence in both extraction and processing capabilities and stringent regulatory policies are positioning it as the central nervous system of the global mining industry.

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalData

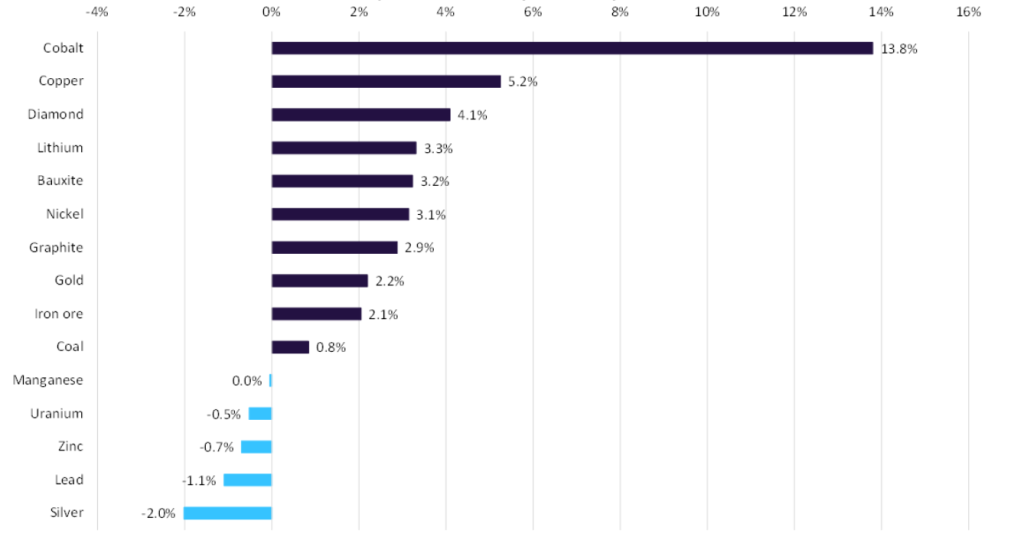

Through to 2030, China’s mining sector presents a highly divergent outlook across key commodities. Growth is predominantly concentrated in critical minerals, with steady CAGRs projected for lithium (3.3%), graphite (2.9%), and uranium (2.1%), driven by strategic expansions and new projects. Among the base metals segment, copper production leads with a 2.0% CAGR due to ongoing mine expansions, while zinc, lead, manganese and iron ore output is largely expected to remain flat due to the absence of significant net capacity additions or balancing closures with new project commencements. In contrast, precious metals and certain other resources face headwinds; gold production is forecast to slightly decline at a negative 0.2% CAGR, due to scheduled mine closures, and bauxite output is also anticipated to decrease due to the closure of several bauxite mines, mainly in the Shanxi and Henan provinces, following stricter environmental regulations.

India continues to play a leading role in the Asia Pacific’s mining landscape, particularly in coal and iron ore. The country accounted for 16.3% of the region’s coal production in 2024, supported by major operators including Coal India and the Singareni Collieries. Coal output in India is projected to grow by 5.2% through the outlook period to 1,511.2mt by 2030, owing to the government’s strategy of auctioning coal blocks to private companies for mining purposes. India’s Ministry of Coal is targeting Atma-Nirbhar (self-reliance) in coal by rapidly expanding domestic production capacity. It plans to open 100 new mines by FY2029-30 to add 500mtpa, with 13 mines already operationalised in FY2024-25 (83mt capacity) and over 20 more planned in FY2025-26. Meanwhile, India’s iron ore production is expected to grow at a CAGR of 2.7% through 2030, owing to increased domestic steel demand from infrastructure and manufacturing sectors, a rise in investment, and supportive government policies.

Over the forecast period, the trajectory of several key minerals other than coal and iron ore in India is anticipated to show negative growth, driven by a wave of scheduled mine closures and an absence of new capacity additions. This trend points to significant contractions across key base and precious metals output. The most severe impacts are projected for silver, zinc, and uranium production, which face substantial negative CAGRs of 18.9%, 7.5%, and 10.1% respectively, tied to the closure of major operations such as the Kayad, Sindesar Khurd, and uranium mines such as the Banduhurang, Turamdih, Narwapahar and Bhatin. Lead output is also anticipated to fall. Meanwhile, the segments offering stability or minimal expansion are limited to bauxite, which forecasts only marginal growth at a 1.1% CAGR, and manganese, where supply is expected to remain flat through 2030 due to a lack of new investment in capacity.

Indonesia also plays a leading role in the Asia Pacific’s critical mineral output, particularly nickel and cobalt. The country accounted for 80.2% of the region’s nickel production in 2024, supported by major operators including PT Bumi Resources, PT Alamtri Resources Indonesia and PT Bayan Resources. Nickel has the highest strategic value, with Indonesia accounting for over half of the global nickel production and is expected to continue its dominance in the coming years.

Indonesia accounts for the world’s largest nickel reserves, and its efforts to leverage this mineral through government policies are driving the nickel industry. Through to 2030, Indonesia’s nickel supply is forecast to grow by a 3.9% CAGR, due to the planned start of new capacity additions. Meanwhile, Indonesia accounted for 82.4% of the region’s cobalt output in 2024, and the country’s cobalt output is expected to grow by 15.6% CAGR through 2030, mainly due to the planned start of projects including the Pomalaa, Morowali (2026) and Sorowako Limonite Ore project in 2027.

Beyond China, India and Indonesia, the Philippines also plays a key role in the Asia Pacific’s mining landscape. The Philippines’ mining sector is currently undergoing regulatory reforms to create a simplified and balanced tax system for large-scale metallic mining. A key milestone was the signing of the Republic Act No. 12253 on 4 September 2025, introducing the Enhanced Fiscal Regime for Large-Scale Metallic Mining. The law ensures the government gets a fair share of revenues, while reinforcing transparency, accountability and governance. The law also promotes sustainable mining practices, a simplified permitting process and emphasises value-added processing over raw ore export.

The Philippines holds notable nickel and cobalt reserves. The country accounted for 14.9% of the Asia Pacific’s nickel output in 2024 (9.7% globally). However, nickel production is expected to remain flat through the forecast period, due to the planned mine closures and depletion of ore reserves. The country also contributed 10.9% of Asia Pacific’s cobalt production in 2024 (just 1.3% of global supply), and through to 2030, the Philippines’ cobalt supply will remain flat due to the absence of any capacity additions.

Asia Pacific mineral production CAGR by commodity

Content Original Link:

" target="_blank">