Bunker indices move in different directions

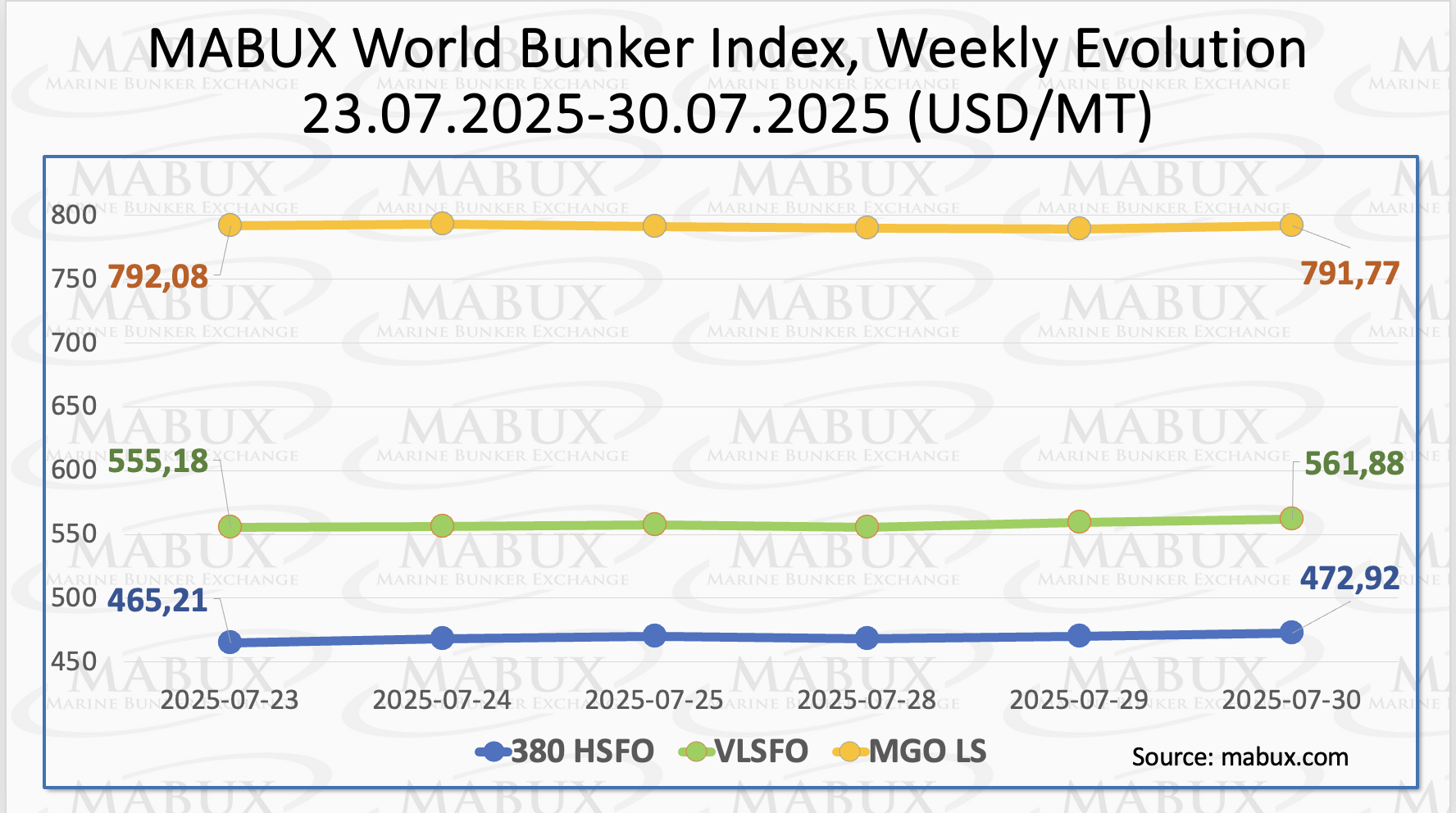

Global bunker indices tracked by Marine Bunker Exchange (MABUX), continued to move in different directions. The 380 HSFO index rose by US$7.71, gradually approaching the US$500.00 threshold.

The VLSFO index also showed growth, climbing by US$6.70, to US$561.88/MT. In contrast, the MGO index declined slightly by US$0.31, although it still remains near the US$800 mark.

”There are signs of a resumption of the upward trend in the global bunker market,” said Sergey Ivanov, Director, MABUX.

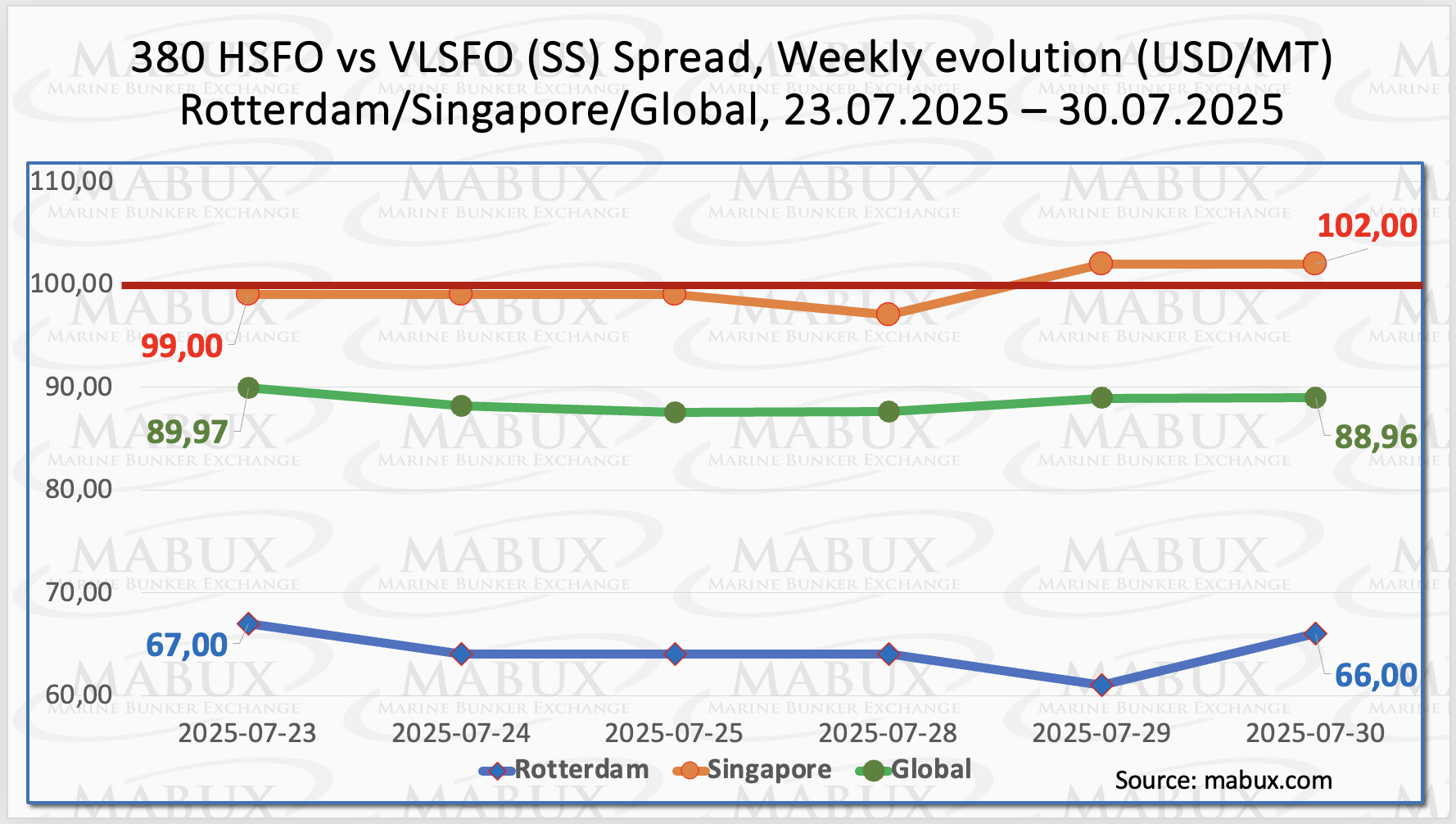

The MABUX Global Scrubber Spread (SS) continued its moderate decline, dropping by US$1.01, remaining below the psychological US$100.00 breakeven mark (SS Breakeven). The weekly average of the global index also fell by US$1.88. In Rotterdam, the SS Spread decreased by another US$1.00, while the weekly average in the port declined by US$1.84.

Conversely, in Singapore, the price difference between 380 HSFO and VLSFO increased by US$3.00, once again surpassing the US$100.00 threshold. However, the weekly average in the port still fell by US$1.66.

”The mixed dynamics of the SS Spread indices illustrate the current transitional state of the bunker market, which is gradually working toward establishing a sustainable trend. For now, the use of conventional VLSFO fuel continues to offer greater profitability than the combination of HSFO and scrubber technology,” commented Ivanov.

According to the International Energy Agency (IEA), global natural gas demand growth is projected to slow from 2.8% in 2024 to about 1.3% in 2025. However, demand is expected to rebound in 2026, accelerating to around 2% as expanding LNG supplies—particularly from the United States, Canada, and Qatar—boost availability and drive higher consumption in Asia.

LNG output is forecast to grow by 7% in 2026, marking the largest annual increase since 2019. The IEA notes that these projections come amid heightened uncertainty in the global macroeconomic outlook and geopolitical instability. The agency continues to monitor gas markets closely and engage with stakeholders to ensure supply security.

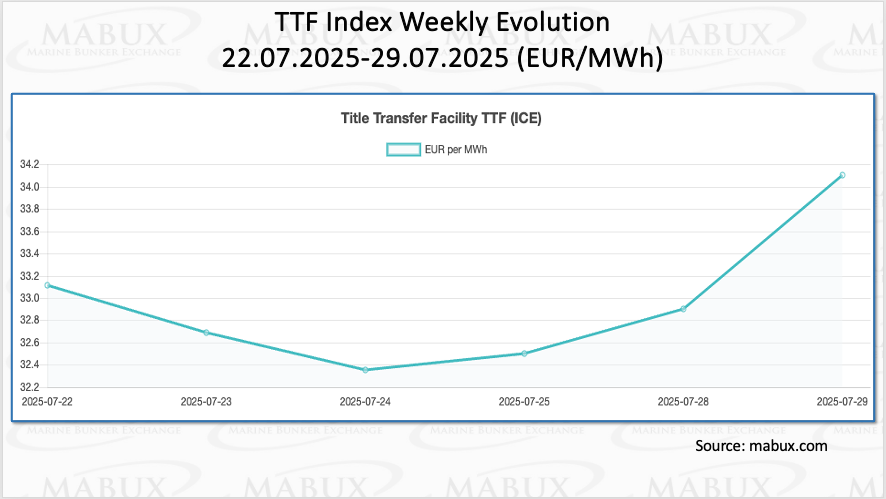

As of July 29, European regional gas storage facilities were 67.63% full, marking an increase of 2.21% compared to the previous week but a decline of 3.70% from the beginning of the year, when storage levels stood at 71.33%. The gas injection process in the European Union remains ongoing as the region prepares for the coming heating season. At the end of Week 31, the European gas benchmark TTF recorded a price increase of 0.992 euros/MWh, rising from 33.111 euros/MWh the previous week to 34.103 euros/MWh.

The price of LNG as a bunker fuel in the port of Sines (Portugal) dropped by another US$ 57 by the end of the week, reaching US$752/MT. Meanwhile, the price difference between LNG and conventional fuel remained favorable for LNG. As of July 28, the gap widened to US$40 in favor of LNG, up from just US$3 the week before. On the same day, MGO LS was quoted at US$792/MT in the port of Sines.

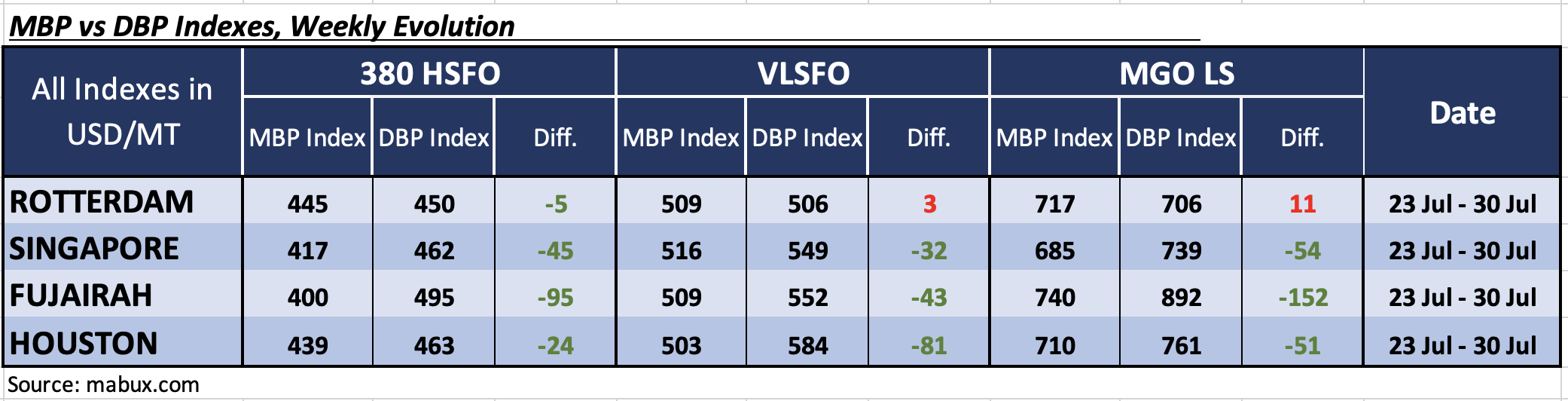

At the end of Week 31, the MABUX Market Differential Index (MDI), which reflects the ratio between market bunker prices (MBP) and the MABUX Digital Bunker Benchmark (DBP), showed mixed trends in average weekly bunker prices across the world’s major hubs—Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: All ports remained in the undervalued zone. MDI values declined by 2 points in Rotterdam and by 3 points in Houston, while increasing by 4 points in Singapore and 3 points in Fujairah. Notably, Rotterdam’s MDI approached the 100% correlation mark between MBP and DBP.

• VLSFO segment: Rotterdam was the only port that remained overvalued, with its MDI index falling by 1 point yet still holding near the 100% correlation level. The other three ports—Singapore, Fujairah, and Houston—continued to show undervaluation. MDI levels rose by 4 points in Singapore and by 5 points in Fujairah but dropped by 8 points in Houston.

• MGO LS segment: Rotterdam again stood out as the only overvalued port, with its MDI increasing by 8 points. The remaining ports—Singapore, Fujairah, and Houston—were all undervalued. MDI values rose slightly by 1 point in Singapore and Houston, while decreasing by 1 point in Fujairah, where the index still remained above the US$100.00 mark.

Overall, there were no substantial changes in the pattern of overvalued and undervalued ports by the end of the week.

”The global bunker market continues to be characterized by a dominant trend toward fuel undervaluation, and there are currently no signs indicating a shift in the prevailing MDI dynamics,” stated Sergey Ivanov, Director, MABUX.

”The current geopolitical and global economic landscape—particularly the potential introduction of increased import tariffs in the United States—has the potential to trigger a renewed upward trend in global bunker prices. Based on current indicators, we anticipate that bunker indices may experience moderate growth in the coming week,” added Ivanov.

The post Bunker indices move in different directions appeared first on Container News.

Content Original Link:

" target="_blank">