Global bunker prices keep falling

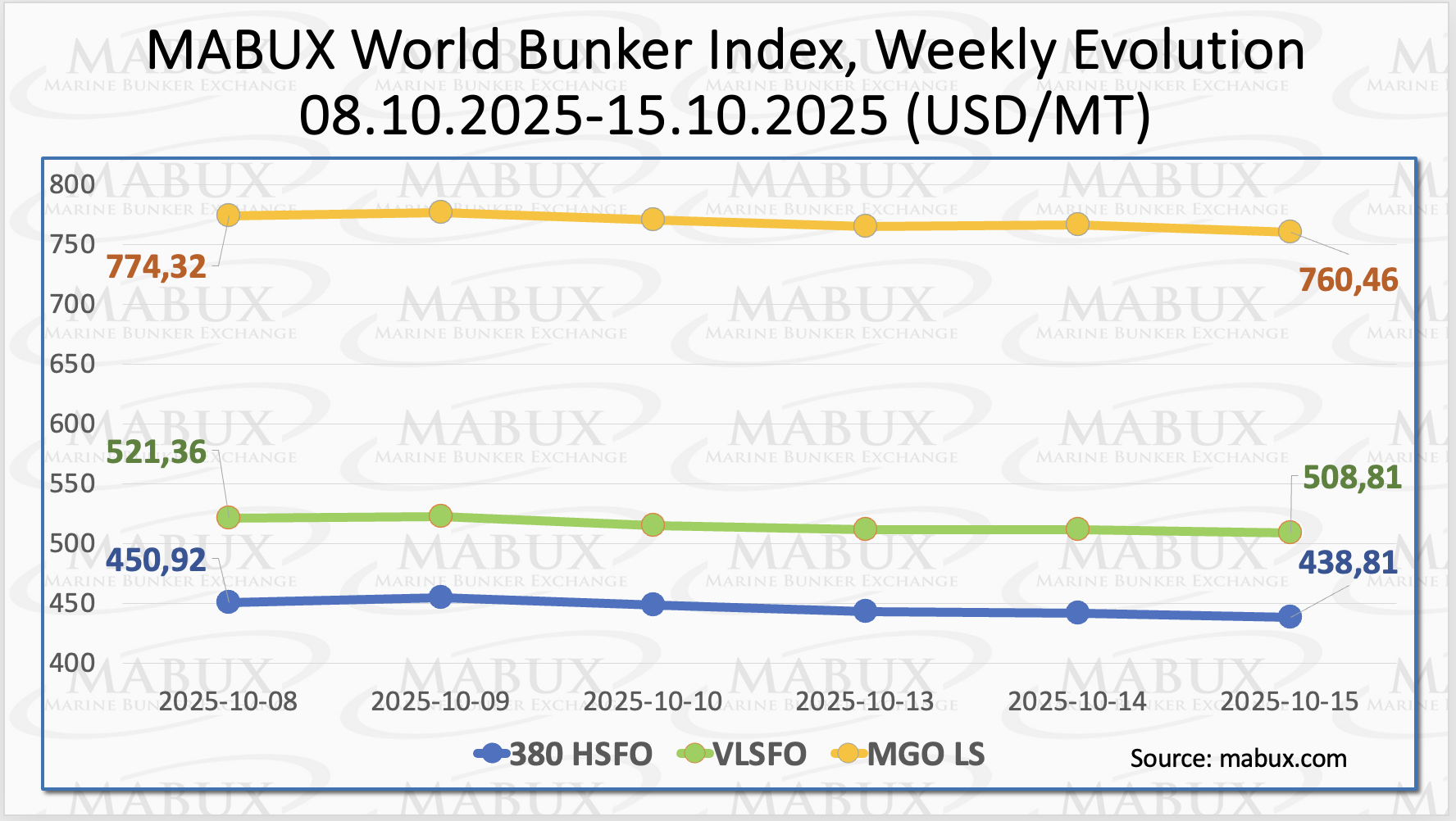

At the end of the 42nd week, global bunker indices MABUX continued their downward trajectory, defying expectations of an upward correction. The 380 HSFO index declined by US$12.11, to US$438.81/MT, slipping below the US$450 threshold.

The VLSFO index dropped by another US$12.55, reaching USD 508.81/MT, approaching the US$500 level. The MGO index also decreased by US$13.86, moving to US$760.46/MT. At the time of writing, a moderate downward trend persisted across the global bunker market.

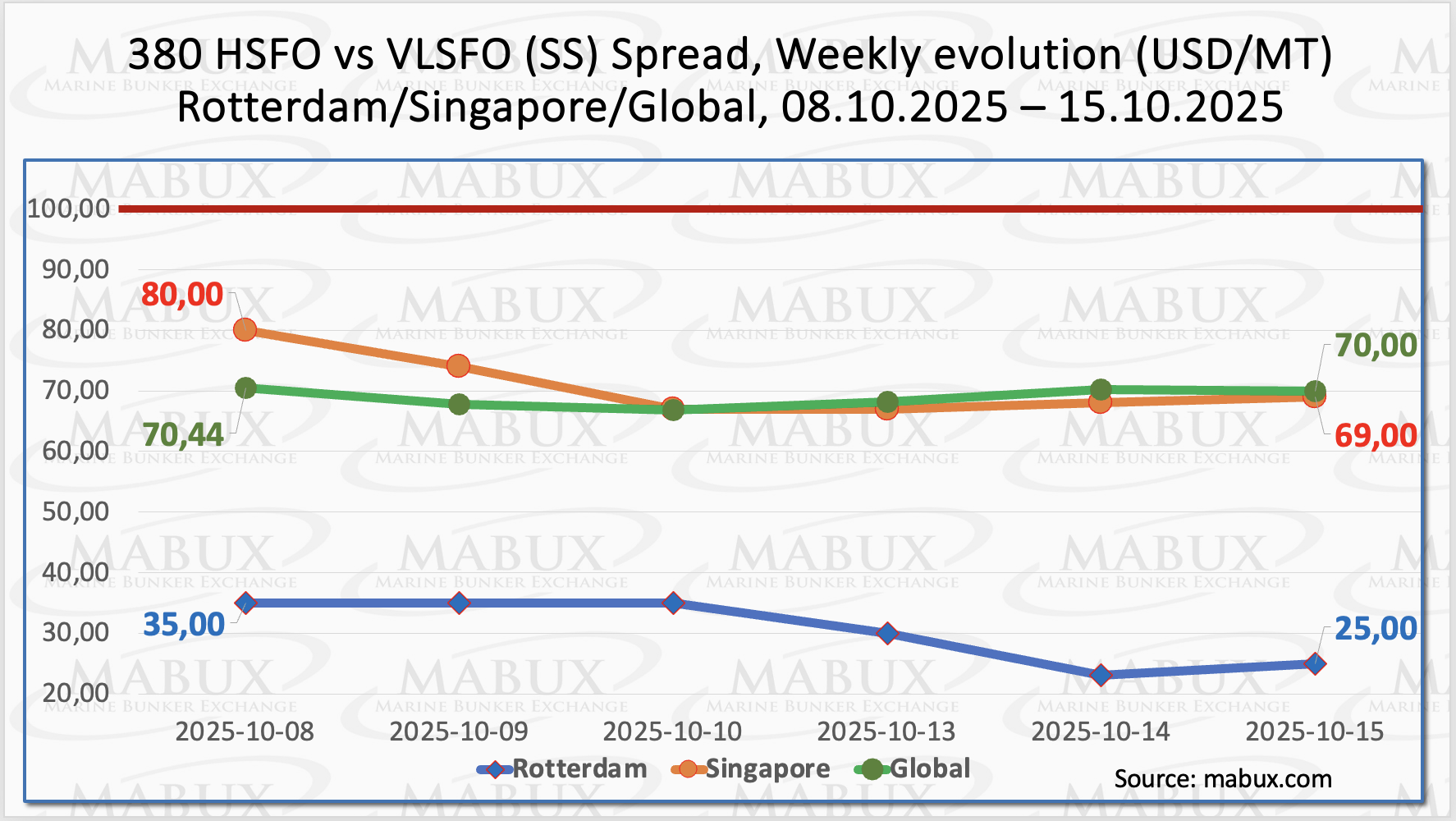

The MABUX Global Scrubber Spread (SS) — the price difference between 380 HSFO and VLSFO — posted a slight decline of US$0.44, moving to US$70.00. The indicator remains well below the psychological breakeven level of US$100.00. The weekly average of the index also decreased by US$2.68.

In Rotterdam, the SS Spread continued its downward movement, losing US$10.00 to settle at US$25.00 compared to US$35.00 a week earlier, reaching a low of US$23.00 at one point — the first time since October 30, 2024.

The weekly average in the port fell by US$10.00. In Singapore, the 380 HSFO/VLSFO price spread narrowed by US$11.00, from US$80.00 to US$69.00, while the weekly average slipped by US$1.50.

Overall, SS Spread indicators declined steadily throughout the week, further widening the gap from the US$100.00 psychological mark and reinforcing the cost advantage of using conventional VLSFO over the HSFO + scrubber option. This downward trend is expected to persist into next week.

Forecasts indicate that demand for liquefied natural gas (LNG) as a marine fuel could at least double by 2030, driven by stricter emissions standards and a growing fleet of LNG-capable vessels. Large-scale export projects in the US and Qatar are expected to result in an LNG oversupply by the end of the decade, putting downward pressure on prices and enhancing its cost competitiveness relative to traditional, higher-emission bunker fuels.

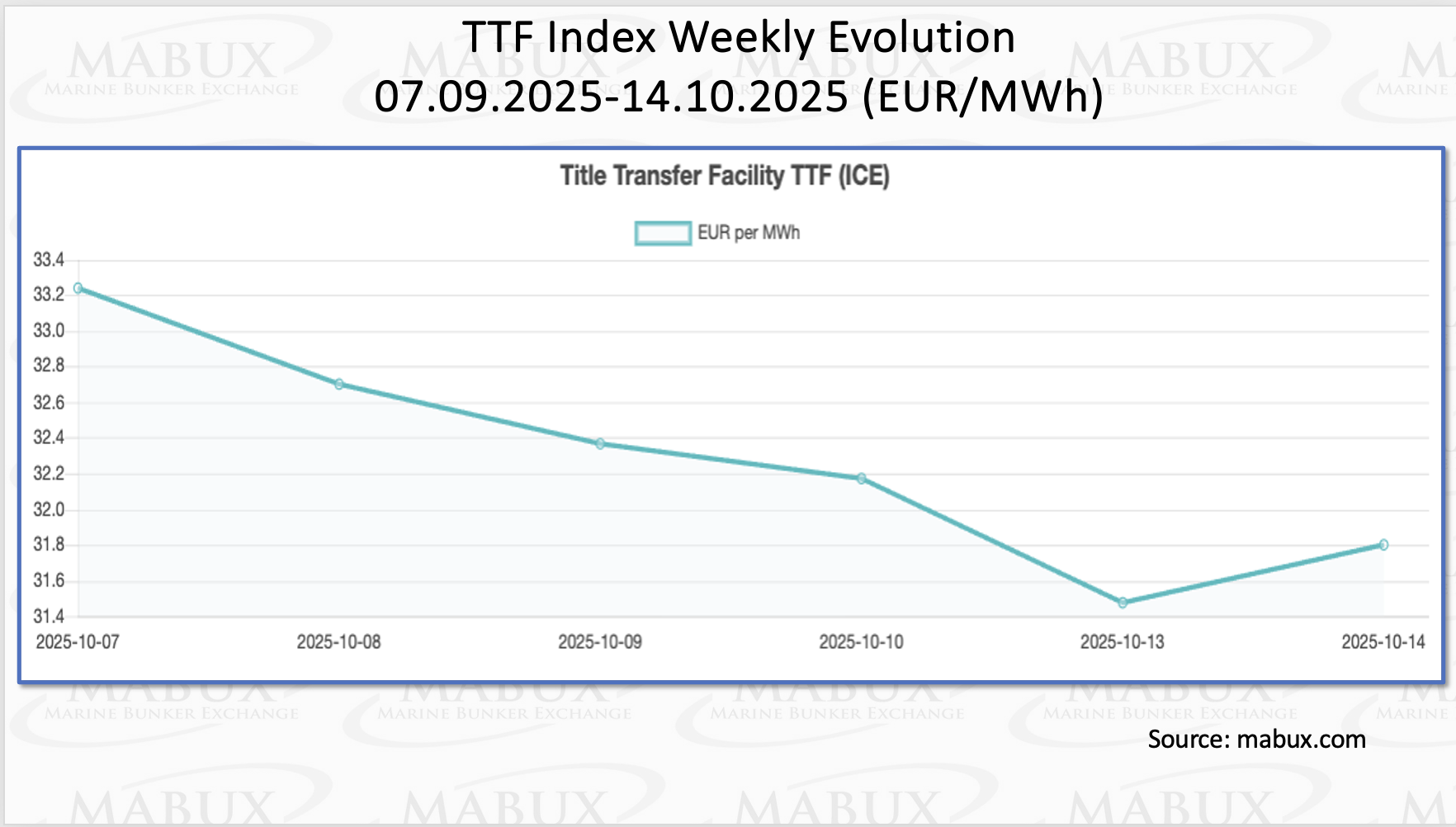

As of October 14, European regional gas storage facilities were 83.09% full, reflecting a 0.54% increase compared to the previous week. This level is 11.76% higher than at the beginning of the year (71.33%), although the pace of injections remains relatively modest. By the end of the 42nd week, the European TTF gas benchmark continued its downward trend, declining by €1.445/MWh to €31.801/MWh, compared to €33.246/MWh a week earlier.

The price of LNG as a bunker fuel at the port of Sines (Portugal) continued its downward trend this week, falling by USD 36.00 to USD 732/MT, compared to USD 768/MT the previous week. The price differential between LNG and conventional fuel also narrowed, reaching just USD 10 in favor of conventional fuel—down from USD 32 a week earlier. On the same day, MGO LS was quoted at USD 722/MT at the port of Sines.

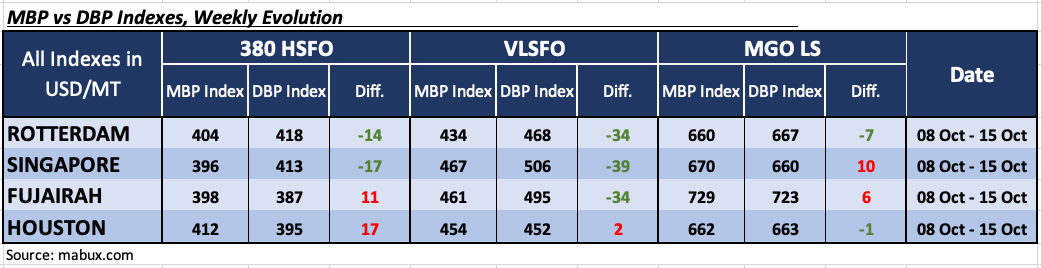

At the end of the 42nd week, the MABUX Market Differential Index (MDI)—the ratio of market bunker prices (MBP) to the MABUX digital bunker benchmark (DBP)—reflected the following price dynamics across the world’s largest hubs: Rotterdam, Singapore, Fujairah, and Houston:

- 380 HSFO segment: Fujairah and Houston remained overvalued, with their average weekly MDI values rising by 4 and 5 points, respectively. In contrast, Rotterdam and Singapore stayed undervalued, with MDI values falling by another 8 and 7 points, respectively.

- VLSFO segment: Houston was the only overvalued port in this segment, although its average MDI decreased by 5 points, moving closer to the 100% MBP/DBP correlation mark. All other ports remained undervalued. Average weekly MDI values were unchanged in Rotterdam, while they increased by 8 points in Singapore and 15 points in Fujairah.

- MGO LS segment: Singapore and Fujairah shifted into the overvalued zone, with MDI values rising by 10 and 17 points, respectively. Rotterdam and Houston remained undervalued, with MDI values declining by 8 and 2 points. Notably, the MDI values for Rotterdam, Fujairah, and Houston are currently close to the 100% MBP/DBP correlation threshold.

”By the end of the week, the overall balance between overvalued and undervalued ports continued to tilt toward overvaluation. Currently, two ports are overvalued in both the 380 HSFO and MGO LS segments, and one port is overvalued in the VLSFO segment. This trend suggests a gradual structural shift in the MDI balance toward overvaluation, which is expected to persist in the coming week”, commented Sergey Ivanov, Director, MABUX.

”We believe that the moderate decline in bunker indices is set to continue, with the downward trend expected to extend into next week”, added Ivanov.

The post Global bunker prices keep falling appeared first on Container News.

Content Original Link:

" target="_blank">