Global MABUX bunker indeces show mixed movements

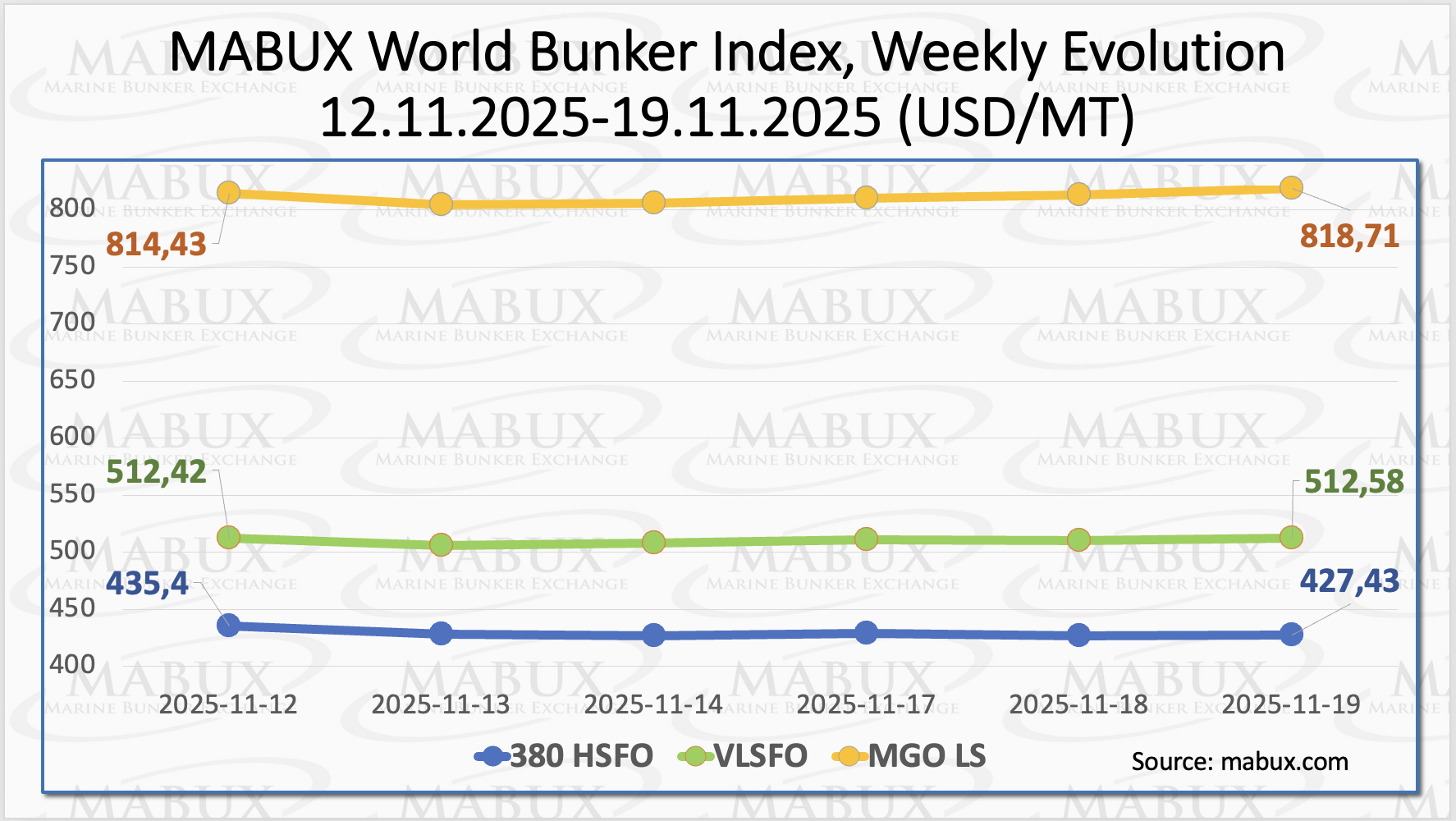

Based on the results of Week 47, the global MABUX bunker indices remained in a phase of mixed, multidirectional movement. The 380 HSFO Index declined by US$7.97, falling to US$427.43/MT and breaking below the US$430 threshold.

In contrast, the VLSFO Index posted a marginal increase of US$0.16 (512.58 USD/MT versus 512.42 USD/MT a week earlier). The MGO LS Index also edged higher, adding US$4.28 to reach UD$818.71/MT. At the time of writing, the global bunker market continued to demonstrate diverging price movements with no clearly defined trend.

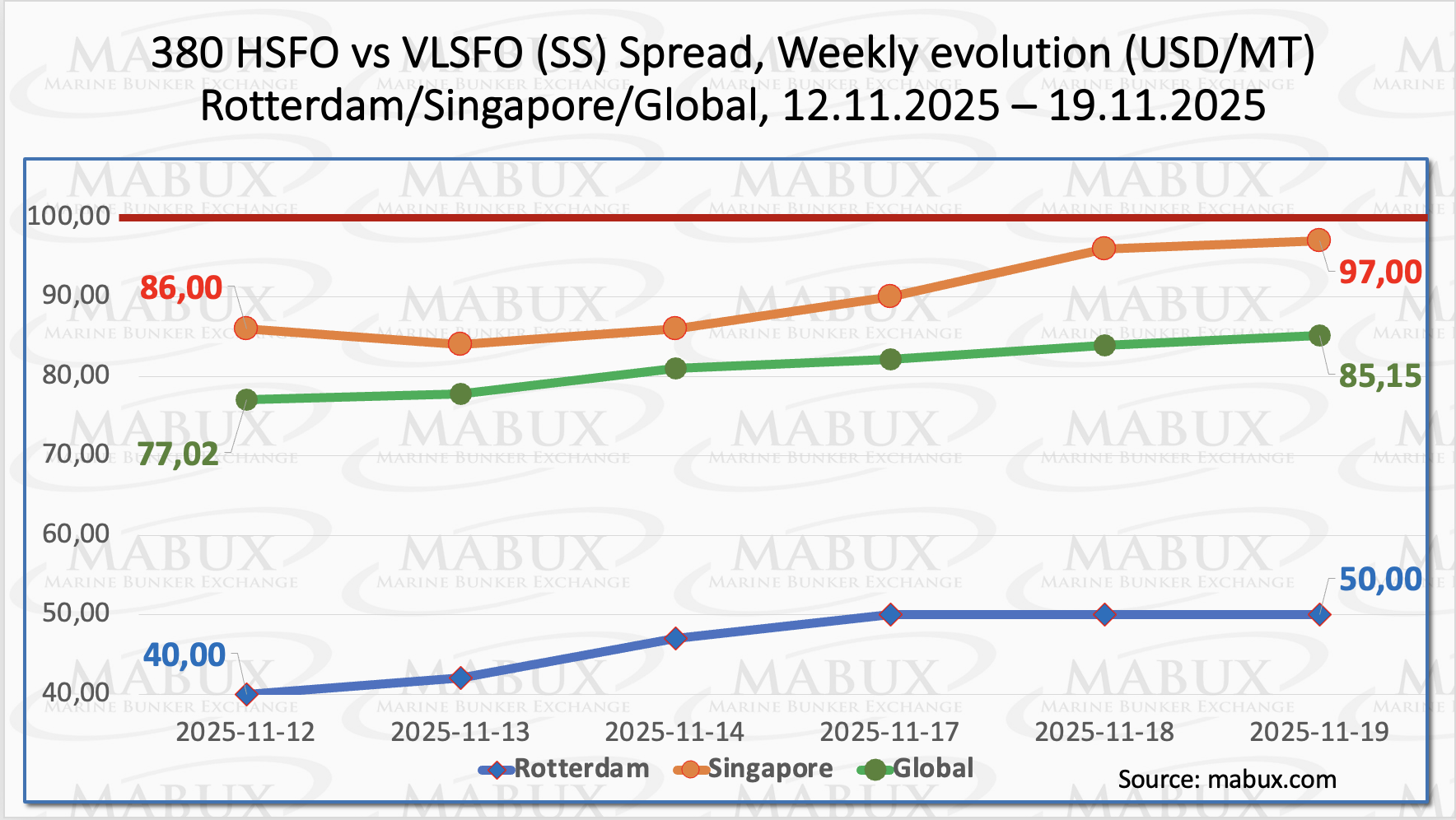

The MABUX Global Scrubber Spread (SS) — the price differential between 380 HSFO and VLSFO — continued its upward trajectory, increasing to US$85.15, thereby surpassing the US$80.00 threshold. The weekly average of the index also rose by US$8.21. In Rotterdam, the SS Spread extended its gains, adding US$10.00.

The port’s weekly average likewise strengthened, rising by US$12.00. In Singapore, the price gap between 380 HSFO and VLSFO widened by US$11.00, to US$97.00), moving close to the psychological US$100.00 level (SS Breakeven).

The weekly average in the port also increased by US$7.66. The continued expansion of the 380 HSFO–VLSFO price differential suggests a sustained upward trend in the SS Spread. We anticipate that the index may reach — and potentially exceed — the US$100.00 mark next week, further shifting the profitability balance in favor of the HSFO + Scrubber option over conventional VLSFO.

According to Kpler, LNG imports to Asia in October totaled 22.84 million tons, marking a slight increase from September but remaining noticeably below the 24.39 million tons recorded in October 2024. Over the first ten months of 2025, Asia’s cumulative LNG imports declined by more than 14 million tons year-on-year, amounting to 225.8 million tons.

A key driver behind this contraction was China, which has reported year-on-year declines in LNG imports every month since November 2024. In contrast, European LNG inflows continued to rise. During the same period, Europe imported 101.38 million tons, an increase of 16.75 million tons compared to a year earlier — despite EU leadership’s rhetoric about permanently curbing natural gas consumption.

Meanwhile, the Institute for Energy Economics and Financial Analysis (IEEFA) cautioned that European countries risk over-reliance on a single supplier should they continue committing to long-term U.S. LNG contracts. The United States accounted for more than 57% of Europe’s LNG imports in the first half of 2025, consolidating its position as the region’s dominant supplier.

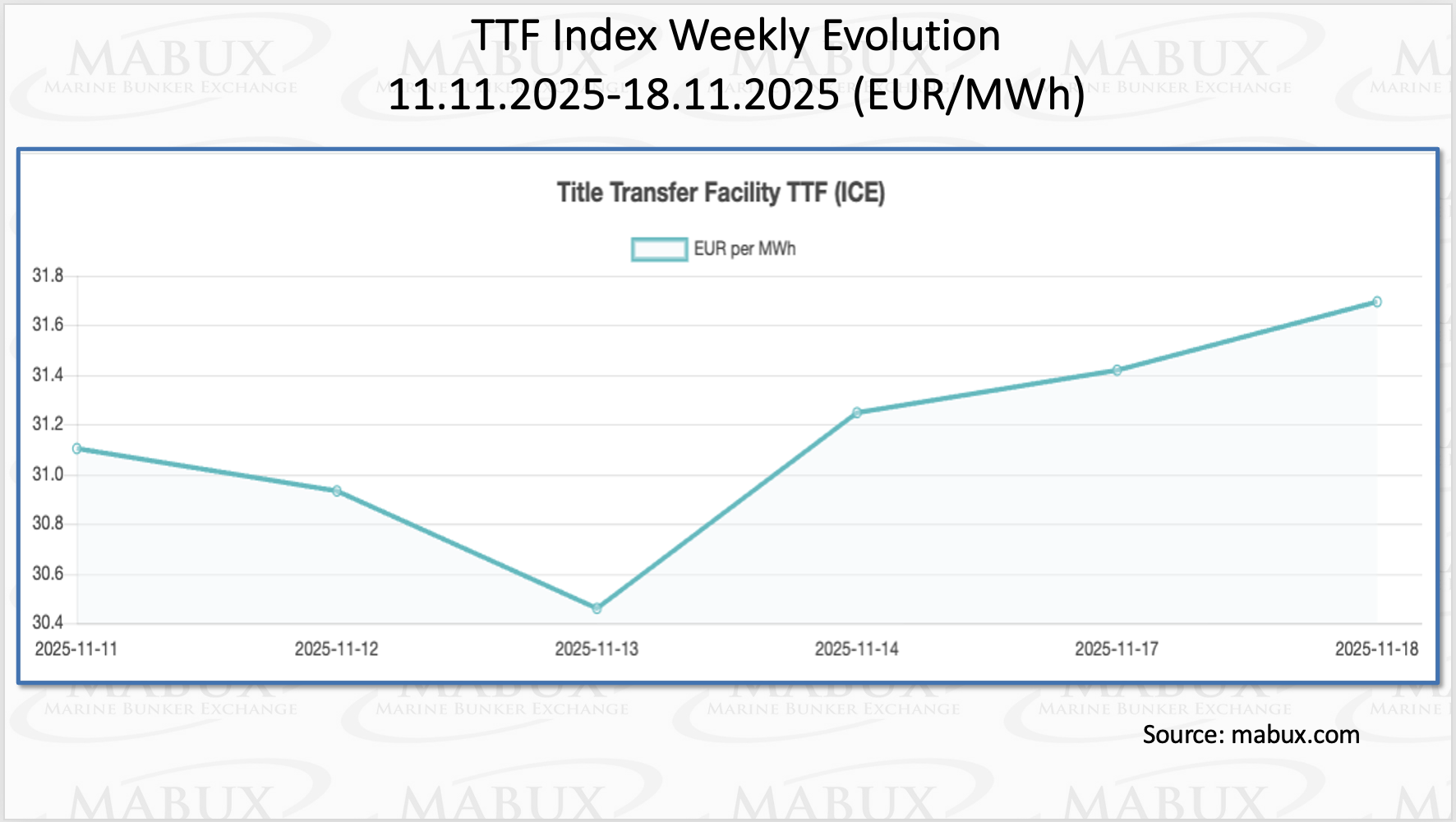

As of Nov. 18, European regional gas storage facilities were 81.68% full (down 0.71% from the previous week). Gas withdrawal rates continue to slightly exceed the rate of storage capacity filling. Filling levels are 10.35% higher than the level at the beginning of the year (71.33%). At the end of the 47th week, the European TTF gas benchmark showed a slight increase: plus 0.592 €/MWh (31.694 €/MWh versus 31.102 €/MWh last week).

The price of LNG as bunker fuel at the port of Sines (Portugal) rose by US$39.00 week-on-week, reaching US$769/MT compared to US$730/MT previously. The LNG–MGO price advantage remained in place, although it narrowed to US$54/MT from US$83/MT a week earlier, with MGO LS quoted at US$823/MT at the port of Sines on the same date.

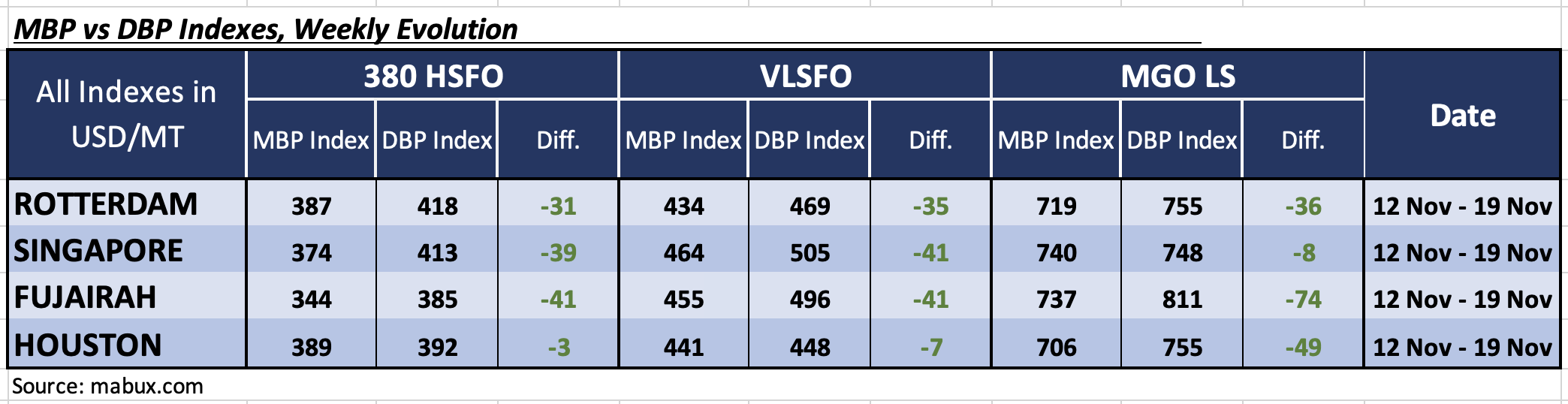

By the end of Week 47, the MABUX Market Differential Index (MDI) — which reflects the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP) — showed a clear predominance of undervaluation across all bunker fuel grades in the world’s major hubs: Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: Houston returned to the undervalued zone, resulting in all four ports being undervalued. Average weekly MDI values increased by 15 points in Rotterdam, 11 points in Singapore, 10 points in Fujairah, and 14 points in Houston. Houston’s MDI is now close to the 100% correlation mark between MBP and DBP.

• VLSFO segment: Average weekly MDI undervaluation levels increased by 1 point in Rotterdam, 3 points in Singapore, 6 points in Fujairah, and 1 point in Houston. Houston’s MDI remained close to the 100% correlation mark.

• MGO LS segment: Undervaluation levels fell by 16 points in Rotterdam, 8 points in Singapore, and 7 points in Fujairah, but increased by 14 points in Houston. Singapore’s MDI moved closer to the 100% correlation threshold.

At the close of the week, the overall balance of overvalued versus undervalued ports fully shifted into the undervalued zone, with Houston being the last port to enter this category. We expect this undervaluation trend to continue in the global bunker market next week”, commented Sergey Ivanov, Director, MABUX.

Ivanov added that the global bunker market is still in the process of forming a sustainable trend. We expect that next week, global bunker indices will continue to fluctuate in different directions, with no clearly defined trend emerging.

The post Global MABUX bunker indeces show mixed movements appeared first on Container News.

Content Original Link:

" target="_blank">

")