Q4 2025 Container Market Analysis

The following Q4 2025 Container Market Analysis report, was conducted by Dr. Michael Tsatsaronis, Assistant Professor at the Department of Port Management and Shipping, National and Kapodistrian University of Athens, and his research team.

- FREIGHT MARKET

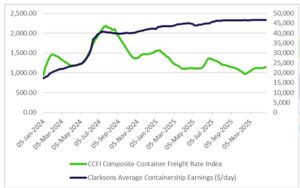

During October, the containership market remained under pressure, as excess vessel capacity and subdued demand continued to influence freight rate levels.

Early in the month, the market showed signs of further weakening, with profitability for liner operators remaining limited. As the month progressed, some indications of stabilization appeared, with a modest improvement observed mid-month.

Towards the end of October, the containership market experienced a slight recovery, although overall conditions continued to reflect a fragile balance, as the effects of increased capacity have not yet been absorbed.

In general, the month highlighted a market still seeking equilibrium between supply and demand, with only limited space for a more sustained improvement in the near term.

During December, the containership freight market was strongly influenced by external factors and geopolitical developments, which shaped an unstable operating environment. References to a potential return of vessels to the Red Sea raised concerns within the market, as such a development is associated with an increase in available capacity and possible pressure on freight rates.

At the same time, toward the end of the year, differences were observed across trade lanes, with certain markets showing signs of strengthening while others remained more restrained. This uneven performance highlighted the absence of a uniform market direction, as developments did not affect all regions in the same manner.

Overall, December reflected a market that remains highly sensitive to changes in shipping routes and to the broader climate of uncertainty surrounding global trade.

- NEWBUILDING – SALES & PURCHASE

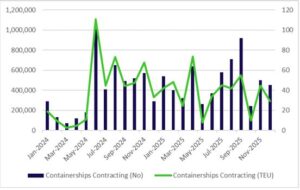

The last quarter of 2025 was of paramount activity. In particular, October included orders from Capital Maritime, Minerva Dry, and Chartworld, while CMA CGM announced the signing of a letter of intent for six new 1700 TEU dual-fuel LNG containerships built in India.

The construction was undertaken by Cochin Shipyard Limited (CSL), and it is noteworthy that six of these ships will be registered under the Indian flag, underlining the company’s commitment to support the Indian economy and maritime growth.

As for Capital Maritime, the Greek seaborn transportation company is willing to expand its fleet by ordering two containerships with a carrying capacity of 1,800 TEUs each at the HD Hyundai Mipo Dockyard (HMD) shipyards (South Korea). Each ship will cost $45 million and is expected to be delivered at the end of 2027.

In parallel, the company exercised its option to build two more containerships, with a carrying capacity of 2,800 TEUs each, at the same shipyards. The construction cost is approximately $55 million per ship, and delivery is also expected at the end of 2027, and all new ships will be equipped with scrubbers.

Furthermore, Minerva Dry placed an order for four new containerships at Penglai Zhongbai shipyards (China) with a carrying capacity of 3,000 TEUs each. The construction will cost $43 million per ship, and they are expected to be delivered in 2027.

Finally, Chartworld ordered eight new containerships at the Yangzhou Guoyu Shipbuilding in China. The new ships are expected to be delivered in 2028, and each of them will have a carrying capacity of 3,100 TEUs.

During October, the sales & purchase market for containerships recorded very limited activity. Only two transactions were completed over the month, involving a 13,000 TEU vessel and a 1,700 TEU feeder, indicating a restrained level of investor engagement in this particular segment.

The subdued pace of transactions suggests that market sentiment remained cautious at a time when other vessel categories demonstrated stronger momentum within the S&P market.

The last month of 2025 ended with a large order from TMG for 10+2 dual-fuel containerships at Zhoushan Changhong International Shipyard (China), with the ships expected to be delivered in 2028.

Overall, new shipbuilding orders for the year reflected the relatively upward trend in freight rates.

With the volatile situation in the Middle East remaining, the increase in tonnage is leading to a need for new shipbuilding and, by extension, an increase in the supply of transport services over the next two to three years.

During December, MSC (Mediterranean Shipping Company) bought four more secondhand containerships. Three of them are Panamax ships ranging between 4,700 and 5,000 TEU. The last one is a smaller vessel around 2,700 – 2,800 TEU.

- DEMOLITIONS

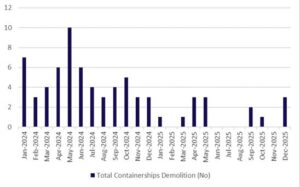

Demolition of containerships has dropped globally to historic lows in 2025: only eight to ten containerships have been scrapped so far this year, compared with 81–82 units in 2023.

Simultaneously, BIMCO estimates that at least 500 containerships (≈ 1.8 million TEU) globally are overdue for recycling—the highest backlog since the 1970s. By 2025 a quarter of the global containership fleet exceeds 20 years old.

Such a sharp drop in containership scrapping despite an aging fleet and record backlog suggests that many older ships will remain in service for the foreseeable future.

Unless demolitions rise dramatically in 2026, the overhang of obsolete capacity risks contributing to oversupply, downward pressure on freight rates, and idle tonnage in the medium term, leading to serious market imbalance within 2027.

Greek shipping outlets echo that demolitions have nearly dried up, partly because owners are keeping older tonnage alive, helped by still-favorable freight income and high second-hand values.

However, if freight markets deteriorate or regulatory pressure increases (e.g., environmental rules), we could see a delayed but sharp wave of scrapping. Analysts argue that to offset the huge orderbook of newbuilds, the industry needs to scrap up to 4.5 million TEU by 2030, a level not seen in decades.

The ship demolition market remained subdued toward the end of the year, with no significant transactions reported specifically for containerships. International ship recycling market analyses indicate that owners showed limited willingness to send containerships for scrapping, reflecting a cautious approach to asset disposal.

The restricted availability of vessels suitable for recycling, combined with generally stagnant market conditions, resulted in a quiet environment with no meaningful developments in this segment.

Written by Dr. Michael Tsatsaronis, Assistant Professor at the Department of Port Management and Shipping, National and Kapodistrian University of Athens, together with his research team: Zacharopoulou Efthimia, Vitzilaiou Anastasia, Skouli Maria Aikaterini, Foteinakis Nikolaos

The post Q4 2025 Container Market Analysis appeared first on Container News.

Content Original Link:

" target="_blank">