Bunker prices extend decline amid ceasefire stabilization

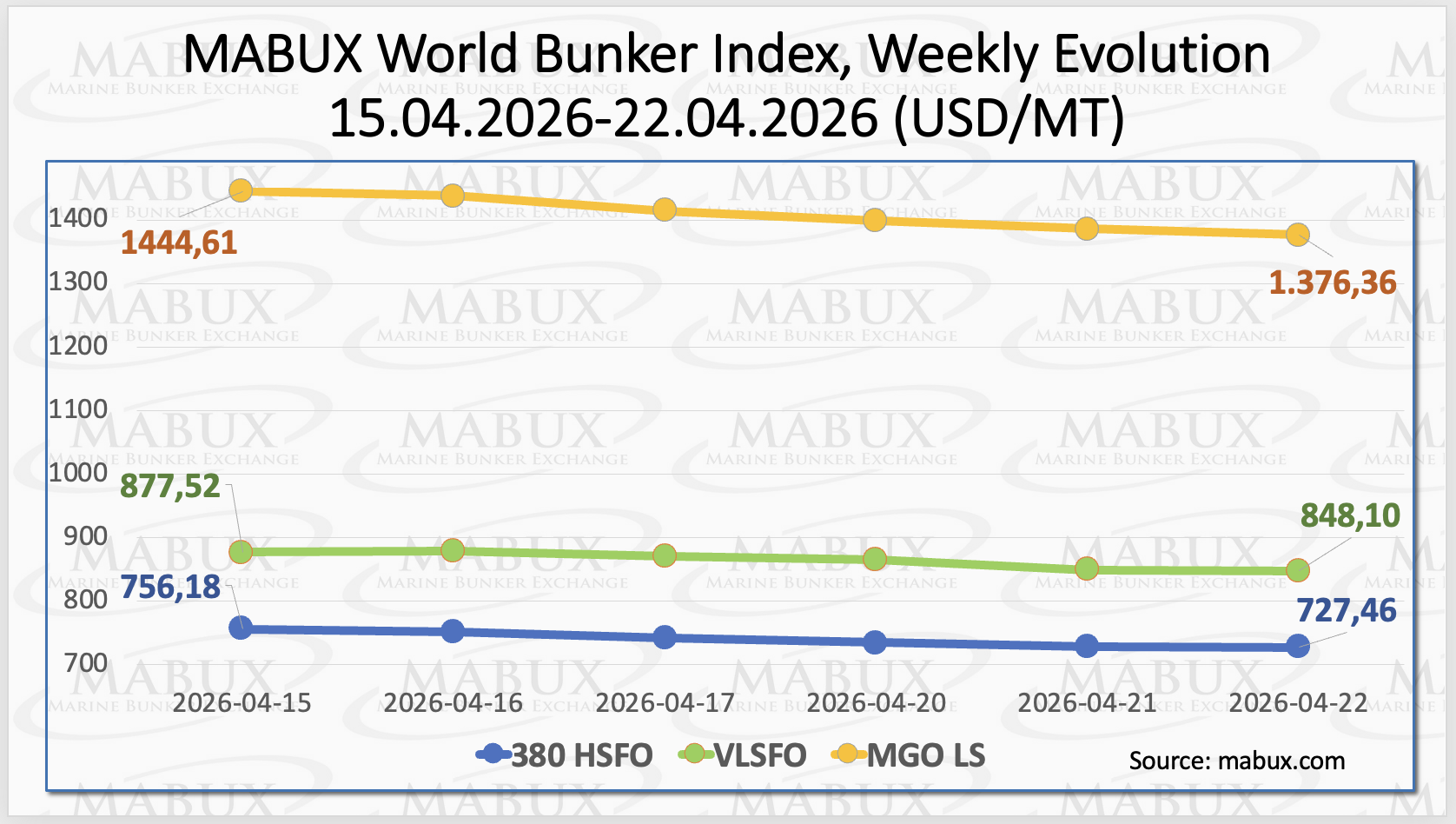

During the week, the global bunker market remained in a downward correction phase, driven by easing geopolitical tensions following the ceasefire in the Middle East, in effect since April 8. By the end of the reporting period, the 380 HSFO index declined by a further US$ 28.2, falling from US$ 756.18/MT to US$ 727.46/MT.

The VLSFO index also continued its downward trajectory, decreasing by US$ 29.42 to US$ 848.10/MT, compared to US$ 877.52/MT the previous week. The most significant drop was observed in the MGO LS segment, which fell by US$ 68.25, from US$ 1,444.61/MT to US$ 1,376.36/MT, breaching the US$ 1,400.00 threshold. MGO LS continues to demonstrate the highest level of volatility within the global bunker market.

At the time of writing, market dynamics indicate a transition to minor and mixed fluctuations, suggesting a potential stabilization phase following the recent correction. “The market is clearly transitioning from a correction phase toward stabilization, although volatility remains elevated,” said Sergey Ivanov, Director, MABUX.

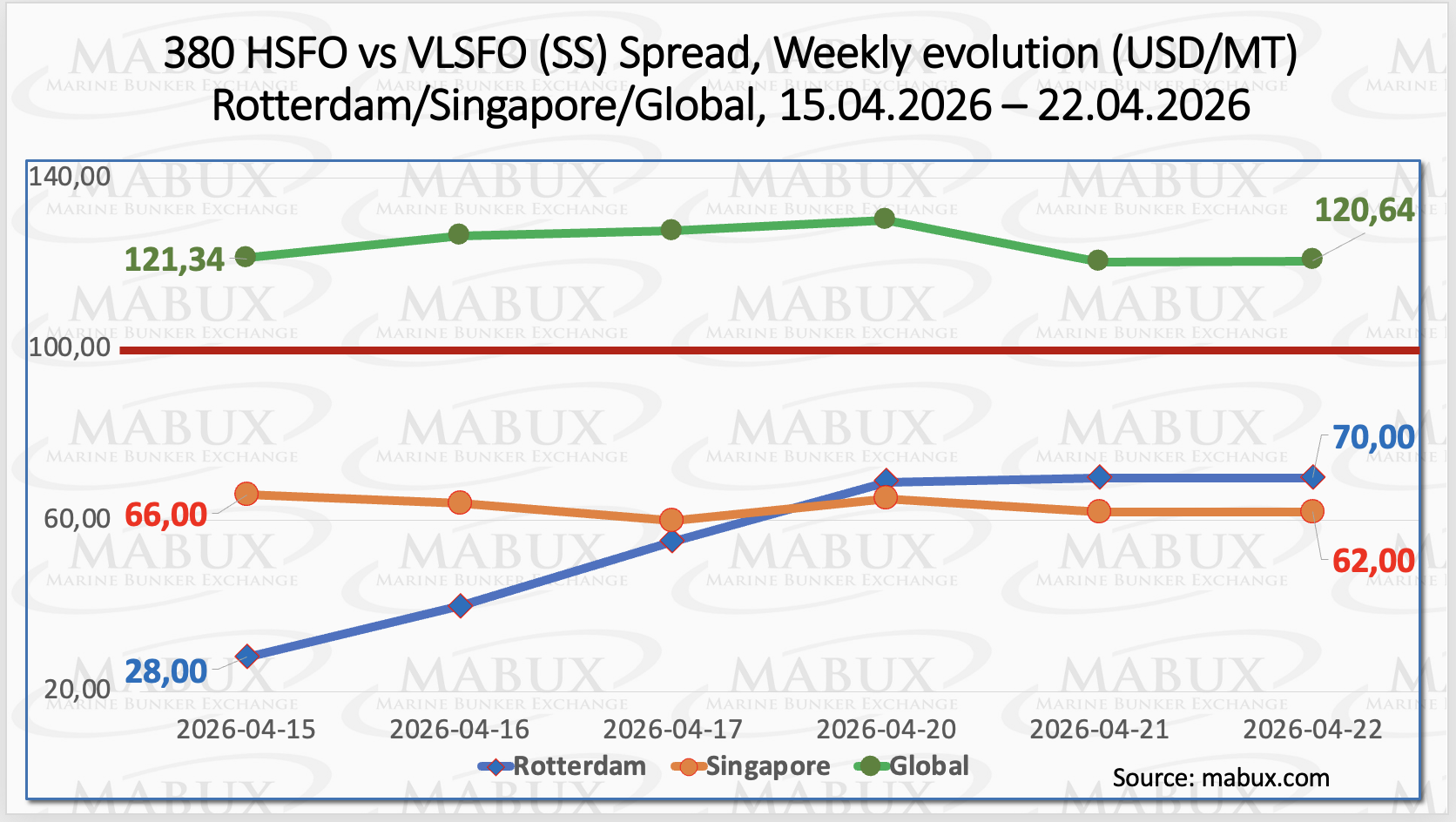

The MABUX Global Scrubber Spread (SS), representing the price differential between 380 HSFO and VLSFO, remained largely stable over the week, declining marginally by US$ 0.70 from US$ 121.34 to US$ 120.64. The index continues to hold firmly above the key psychological threshold of US$ 100.00 (SS Breakeven). Meanwhile, the weekly average of the SS index posted a slight increase of US$ 0.18, indicating relative stability on a broader basis. In Rotterdam, the SS Spread recorded a notable upward movement, rising sharply by US$ 42.00 from US$ 28.00 to US$ 70.00, thus moving closer to the US$ 100.00 breakeven level. The port’s weekly average SS Spread also increased significantly by US$ 26.00. Conversely, in Singapore, the 380 HSFO/VLSFO spread continued to narrow, decreasing by US$ 4.00 from US$ 66.00 to US$ 62.00. The weekly average in Singapore also declined substantially by US$ 35.16.

“Diverging regional dynamics in the scrubber spread highlight uneven supply conditions across key hubs,” Ivanov added.

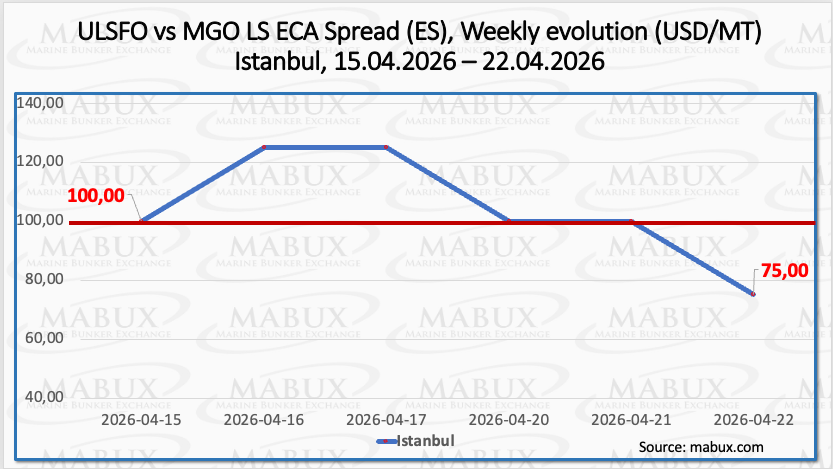

The Istanbul ECA Spread (ES) declined by US$ 25.00 over the week, falling from US$ 100.00 to US$ 75.00 by the close of the reporting period. Despite this net decrease, the index exhibited pronounced intra-week volatility, fluctuating within a wide range of US$ 75–125. The weekly average, however, increased by US$ 8.34. The calculation of the Venice ECA Spread remains temporarily suspended due to the absence of consistent market quotations.

“ECA spreads remain highly sensitive to short-term disruptions and geopolitical risk,” Ivanov commented.

Global gas demand is expected to grow steadily through 2055, supported by expansion in power generation, industry, and transport. LNG is set to play a central role, with seaborne trade projected to double and account for around 65% of global gas flows by mid-century. In the near term, supply disruptions—particularly in the Middle East—are sustaining price volatility and elevated risk premiums, accelerating structural changes in trading strategies and contract structures.

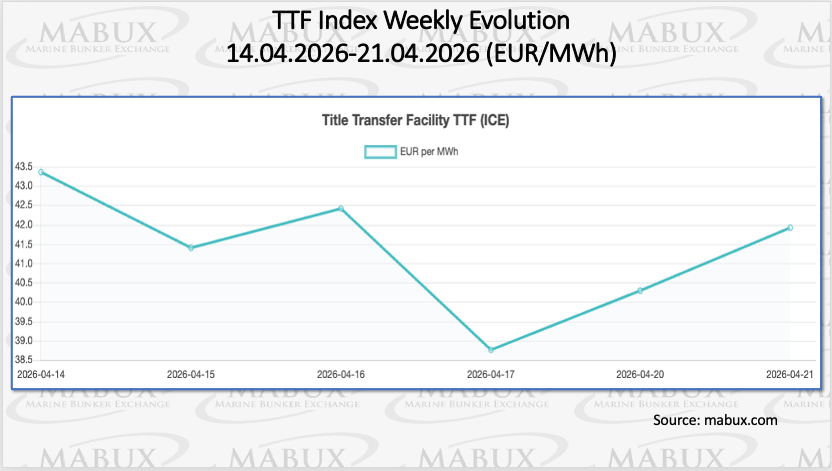

As of April 21, the level of natural gas in European underground storage facilities continued to show a modest increase, reaching 30.61% of total capacity, up by 1.06 percentage points compared to the previous week. However, current storage levels remain significantly lower than at the beginning of the year, standing 29.55 percentage points below the 61.46% recorded on January 1, 2026. At the same time, the European gas benchmark TTF extended its downward trend by the end of week 17, declining by 1,434 euros/MWh to 41,931 euros/MWh, compared to 43,365 euros/MWh the previous week.

The price of LNG as a bunker fuel at the port of Sines (Portugal) continued its downward trend, declining by a further US$ 62.00 over the week to US$ 985/MT, compared to US$ 1,047/MT the previous week. At the same time, the price differential between LNG and conventional marine fuel continued to narrow, reaching US$ 342 in favor of LNG, down from US$ 440 a week earlier. As of April 20, MGO LS at the port of Sines was quoted at US$ 1,327/MT.

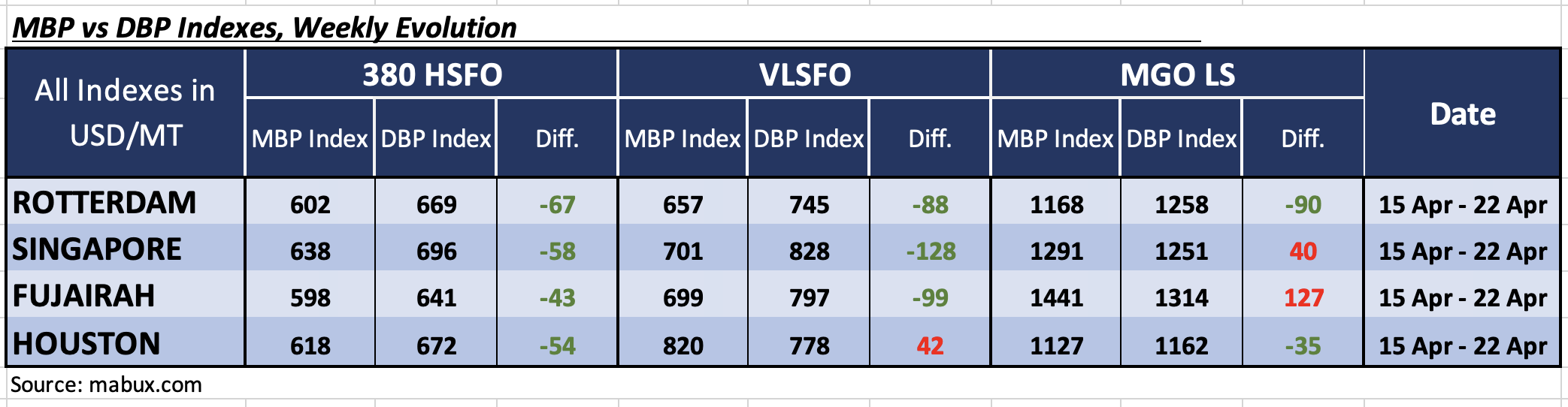

Amid the ongoing geopolitical tensions in the Middle East, the MABUX Market Differential Index (MDI)—reflecting the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP)—continued to display mixed dynamics across Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: All four ports remained in the undervalued zone. The level of discount deepened further in Rotterdam (+13 points), Singapore (+2 points), and Fujairah (+10 points), while Houston recorded a partial correction with the discount narrowing by 25 points.

• VLSFO segment: Houston shifted into the overvalued zone, becoming the sole port in this category, with the premium increasing sharply by 53 points. The other three hubs remained undervalued.

• MGO LS segment: Houston transitioned into the undervalued zone, joining Rotterdam. Singapore and Fujairah remained overvalued, with diverging trends.

“The broader pattern still points toward prevailing undervaluation, despite localized shifts across segments,” Ivanov said.

“This sharp contraction in bunker volumes reflects the direct impact of geopolitical instability on regional demand,” Ivanov noted.

Overall, the global bunker market is undergoing a moderate downward correction while remaining highly sensitive to potential supply-side disruptions. Regional supply-demand balances have shown some improvement, particularly in Singapore, contributing to short-term stabilization. At the same time, persistent geopolitical uncertainty surrounding the Strait of Hormuz continues to represent a significant upside risk for prices.

“We expect continued volatility, with the market reacting quickly to any geopolitical developments,” Ivanov concluded.

The post Bunker prices extend decline amid ceasefire stabilization appeared first on Container News.

Content Original Link:

" target="_blank">