In 2025 to-date, five out of the six liquefaction projects reaching Final Investment Decisions (FID) globally, representing around 90% of liquefaction capacity, are located on the U…

In 2025 to-date, five out of the six liquefaction projects reaching Final Investment Decisions (FID) globally, representing around 90% of liquefaction capacity, are located on the U.S. Gulf Coast. Despite an inflationary environment, geopolitical tailwinds combined with U.S. LNG’s flexibility and relative price competitiveness will accelerate further FIDs in the area over the next 12 months, including NextDecade’s Rio Grande LNG Train 5.

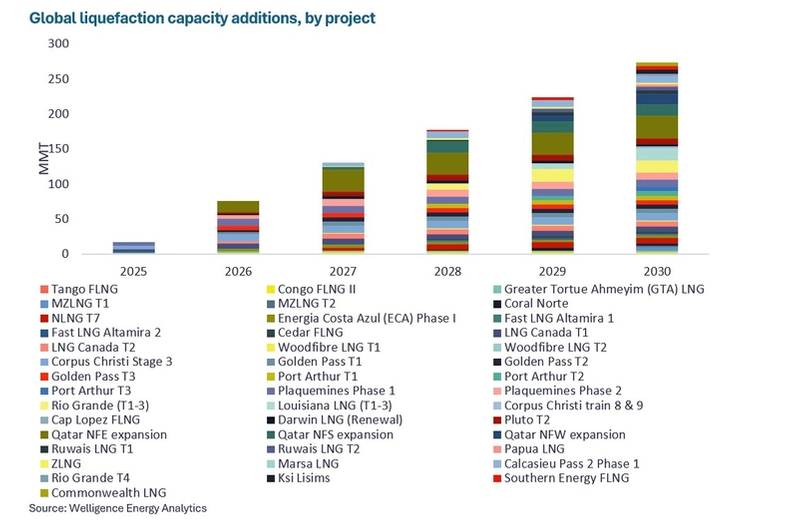

By 2030, the U.S. Gulf Coast will supply over 25% of global LNG production. Asian importers have concerns around high reliance on the area and are accelerating proposed projects elsewhere. Glenfarne Group is leading the proposed Alaska LNG project, from which CPC, PTT, and JERA have signed offtake agreements.

The 20 MMtpa-capacity development is targeted to reach FID in 2026 and benefits from low feed gas costs, much shorter shipping times to Asia, as well as plans to offer buyers a range of price indices. However, players are concerned about Alaska LNG’s cost competitiveness, given the necessary construction of its ~1,300 km gas pipeline.

© Welligence Energy Analytics

© Welligence Energy Analytics

Canadian LNG Re-Energized

Attention is also focused on western Canadian projects, following the government’s reinvigorated commitment to grow markets for the country’s vast gas resources. While the Shell-led LNG

Content Original Link:

" target="_blank">