Shipping Stock Breakdown: April Performance Amid Global Trade Tensions

April 2025 unfolded as a month of high tension and shifting dynamics, as container lines faced simultaneous pressures from geopolitical instability and economic policy shocks.

The sharp escalation of trade protectionism—driven by President Trump’s sweeping new tariffs on Chinese and global imports—sent ripples through global supply chains, while sustained disruptions in the Red Sea continued to affect routing efficiency and freight costs.

In this volatile landscape, container shipping equities responded unevenly, reflecting not only broader market sentiment but also the operational profiles and regional exposures of each company.

- SITC International Holdings Co Ltd (1308)

HK$

HK$

SITC traded down from HK$21.40 to 16.32, then climbed back to 20.90. The early decline was tied to sluggish short-sea trade in East Asia and concerns about regional overcapacity, especially in Chinese coastal ports.

The rebound followed an uptick in intra-Asia volumes and repositioning demand, particularly as exporters adapted to shifting logistics networks. SITC’s strength in feeder services made it a natural beneficiary of cargo redistribution caused by vessel rerouting through safer corridors.

- ZIM Integrated Shipping Services Ltd (ZIM)

US$

US$

ZIM began April at US$15.46, dropped to US$11.71, and closed the month at US$14.47. The stock’s volatility reflected sensitivity to shifting spot rates and ZIM’s exposure to charter costs, which weigh more heavily during weak freight markets.

However, late April saw a sharp recovery, driven by rising rate benchmarks on the Asia–US East Coast corridor. ZIM’s asset-light model allowed it to benefit from tight capacity without bearing the full cost burden of vessel ownership, drawing short-term interest from speculative buyers.

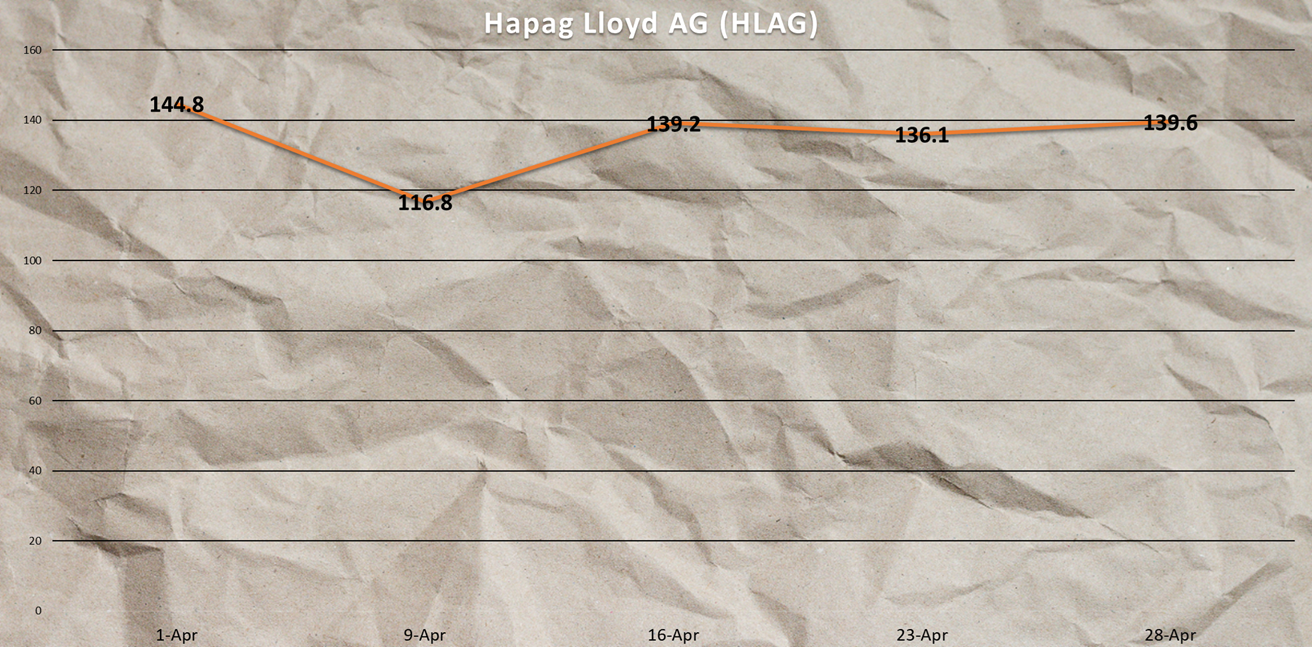

- Hapag Lloyd AG (HLAG)

€

€

Hapag-Lloyd’s stock moved from €114.80 to a mid-month peak of €139.20, finishing slightly lower at €139.60. The strong performance stood out across the sector, reflecting its robust earnings guidance and higher-than-expected spot rate resilience, especially on the Asia–Europe route.

The company benefited from a tighter supply environment caused by longer sailing times due to Red Sea diversions. Investors rewarded its high exposure to premium long-haul container traffic, which was directly impacted by rerouting, enhancing profitability through rising freight surcharges.

- Evergreen Marine Corp Taiwan Ltd (2603)

TWD

TWD

Evergreen slid from TWD 226.50 to 171.00, later recovering to 204.50. Investors reacted early to concerns over extended voyages and potential disruptions in Asia-Europe corridors.

The bounce reflected stabilization in freight indices and a potential bottoming of container spot rates. Evergreen’s strong market presence in Asia-Europe trades helped it benefit from capacity tightening caused by global detours.

- AP Moeller-Maersk AS (AMKBY)

$

$

Maersk saw its stock drop from US$8.65 to US$7.00, then bounce to US$8.30. As a bellwether for global trade, its early dip reflected uncertainty about freight demand and the financial hit from Red Sea rerouting.

A late-month rebound followed reports of stronger-than-expected cargo movement and solid performance in logistics services. Maersk’s end-to-end control of its supply chain played a key role in regaining investor confidence.

- Wan Hai Lines Ltd (2615)

TWD

TWD

Wan Hai declined from TWD 81.90 to 61.10, before jumping back to TWD 82.20. The sharp movement highlighted investor sensitivity to regional shipping dynamics and trade friction in Asia.

By late April, improving intra-Asia trade volumes and higher utilization on feeder services restored confidence. The company’s focus on short-haul and niche lanes proved advantageous under shifting global conditions.

- Yang Ming Marine Transport Corp (2609)

TWD

TWD

Yang Ming’s stock dropped from TWD 77.00 to 56.60, then rose to TWD 69.80. The company faced headwinds from rising operating costs and tensions in the Taiwan Strait, weighing on sentiment.

As the month progressed, improvements in export booking activity and firming charter rates helped fuel a recovery. The rebound pointed to investor optimism that short-term risks would be managed effectively.

- HMM Co Ltd (011200)

₩

₩

HMM’s price declined from ₩20,550 to ₩17,690, ending at ₩18,660. South Korea’s largest container line struggled with rising operating expenses and congestion outside the Red Sea.

Its partial recovery toward month-end was supported by stabilizing freight rates in the Transpacific and intra-Asia lanes. Backing from state-affiliated institutions likely also helped limit downside risk.

- COSCO SHIPPING Holdings Co Ltd ADR (CICOY)

US$

US$

COSCO fell from US$7.87 to US$6.40, with a modest recovery to US$7.11. The early slump was driven by concerns over China’s weak export outlook and operational rerouting via the Cape of Good Hope.

Recovery signs emerged mid-month, supported by Beijing’s easing stance on industrial activity and early signs of cargo volume stabilization. COSCO’s large-scale network also allowed flexibility in vessel redeployment.

- Pan Ocean Co Ltd (028670)

₩

₩

Pan Ocean fell from ₩3,415 to ₩3,065, closing at ₩3,350. Bulk segment softness and reduced South Korean steel exports contributed to early weakness.

Later in April, grain shipments and minor bulks picked up, giving the stock upward momentum. While not highly sensitive to container rate shifts, Pan Ocean remained exposed to the global dry bulk environment.

- Orient Overseas International Ltd (0316)

HK$

HK$

OOIL dropped from HK$116.6 to HK$96.2, finishing the month at HK$109. The early weakness reflected a temporary lull in Chinese export data and market concerns over container imbalances.

OOIL’s late-month recovery followed the strengthening of Asia-US freight indices and greater confidence in Q2 export momentum. As a key player in east-west trade, it benefited from shifting vessel flows and new booking demand.

- Matson Inc (MATX)

US$

US$

Matson’s stock declined steadily from US$131.16 to a low of US$94.50, later recovering to US$106.62. Being heavily dependent on US domestic and Pacific routes, the company was hit early by weaker U.S. retail activity and muted Transpacific bookings.

As April progressed, improved consumer sentiment and stabilizing spot rates on US West Coast lanes helped lift the stock. Matson’s niche market position and integrated logistics offerings added resilience during a volatile month.

- Danaos Corporation (DAC)

US$

US$

Danaos saw a dip from US$79.54 to US$66.47, before ending strong at US$80. The mid-month decline coincided with investor concerns about rising costs associated with rerouting and container repositioning.

However, Danaos’s robust charter book and limited spot exposure allowed it to outperform in the recovery phase. Its rebound was also supported by strong earnings expectations and reduced concerns over operational disruptions.

- MPC Container Ships ASA (MPCC)

₦

₦

MPCC’s stock was highly volatile, fallingfrom ₦ 15.73 on April 1st to ₦13.56, then rebounding to ₦ 15.05 by 28 April. The early weakness reflected soft sentiment in the regional feeder market, combined with ongoing Red Sea disruptions that affected scheduling and fuel costs.

However, the strong recovery later in the month likely resulted from rising short-term charter rates in Europe and intra-Asia due to rerouting and port congestion. MPCC’s focus on smaller vessels made it more reactive to these changes, driving its quick rebound.

- Ningbo Ocean Shipping Co Ltd (601022)

US$

US$

NBOS shares showed notable fluctuation in April, starting at US$8.20, dipping to US$7.29, and closing the month at US$7.75. The early-month decline reflected broader weakness in Chinese-linked shipping equities amid sluggish export momentum and concerns about oversupply in regional container markets.

Toward the end of April, the stock rebounded modestly as container rates stabilized and demand for intra-Asia shipping showed signs of improvement. NBOS, with its operational focus on short- and mid-range Asia-Pacific routes, was able to benefit from cargo rerouting and higher utilization on coastal services. The recovery signaled cautious optimism around Chinese port throughput and shifting regional supply chains.

- Mitsui O.S.K. Lines, Ltd. (9104)

¥

¥

MOL shares fell from ¥5,219 to ¥4,527 mid-month before bouncing to a monthly high of ¥5,272. The early April weakness reflected short-term selling pressure on Japanese exporters and broader equity market dips in Tokyo.

The late recovery was driven by higher demand for LNG shipping and continued earnings strength across MOL’s diversified operations. Red Sea reroutings added value to longer-haul charters, and the weaker yen also helped boost MOL’s competitiveness internationally.

- Nippon Yusen K.K (9101)

¥

¥

NYK’s share price began April at ¥4,914, dipped to ¥4,239 mid-month, and closed near its highs at ¥4,866. The early decline was consistent with the broader pullback in Japanese shipping stocks, triggered by market caution around weaker export orders from Asia and rising bunker fuel costs due to extended rerouting away from the Red Sea.

The recovery in the second half of the month reflected renewed strength in NYK’s car carrier and LNG transport segments, both of which have been outperforming the container divisions. A weaker yen supported export-related income, and the company’s diversified fleet offered resilience during volatile market conditions. Investors responded favorably to NYK’s strategic positioning and multi-segment exposure.

- SFL Corporation Ltd (SFL)

US$

US$

SFL’s stock began April at US$8.22, slipped to a low of US$7.10, and ended the month close to $8.09. The initial weakness aligned with general pressure on shipping stocks due to route disruptions in the Red Sea and rising fuel costs, which disproportionately affect companies with diversified fleets like SFL.

The recovery toward the end of the month likely stemmed from investor confidence in SFL’s long-term charter contracts and exposure to multiple shipping segments, including tankers and rigs. The rebound suggests that markets saw its fundamentals as stable even amid operational uncertainty.

- Kawasaki Kisen Kaisha, Ltd. (9107)

¥

¥

K Line’s stock dropped from ¥2,019 on April 1st to ¥1,624, but steadily recovered to ¥1,995 by the end of the month. The early dip reflected market reaction to weakening export signals from China and global uncertainty in trade routes. However, improving container freight rates, particularly on transpacific lanes, and Japan’s weak yen—which benefits exporters—helped lift the stock.

The company also benefited from stable demand in the auto and LNG shipping segments, while reduced vessel availability globally continued to support rates. Overall, K Line showed solid resilience through April’s volatility.

- Costamare Inc (CMRE)

US$

US$

Costamare started the month strong at US$10.27, but dropped sharply to US$8.37 by April 8th, showing signs of recovery toward US$9.14 by the end of the month. The decline was likely influenced by concerns around global shipping disruptions caused by Houthi attacks in the Red Sea, which increased costs and delays.

Additionally, uncertain demand from Europe and China, combined with tight financing conditions in the US, may have weighed on investor sentiment.

Despite this, the moderate rebound suggests some market confidence in the company’s charter-based model, which offers stability compared to the volatile spot market. Still, lingering geopolitical risks and cautious global trade outlooks continue to affect sentiment.

- The National Shipping Co. (4030)

SAR

SAR

Bahri’s stock moved from SAR ﷼30.85 to a mid-month low of ﷼SAR 29.30, then rebounded to ﷼SAR 30.95. As a major tanker and logistics operator, Bahri was initially pressured by oil market volatility and uncertainty over freight flows through the Gulf region, especially amid increased tensions in the Red Sea and continued Houthi activity.

Despite this, the company’s strategic importance in regional energy transport and its role in Saudi Arabia’s Vision 2030 logistics ambitions helped support its valuation.

The late-April rebound was driven by firmer crude demand, recovery in tanker rates, and broader optimism in the GCC equity markets. Bahri’s steady fundamentals and national significance offered investors a safe exposure to global trade disruptions.

April proved to be a volatile month for container shipping equities, with the majority of companies posting negative returns despite some late recoveries. Standouts like Wan Hai (+0.37%), MOL (+1.02%), Danaos (+0.58%), and The National Shipping Co. (+0.32%) managed to end in the green, reflecting either niche market advantages or diversified exposure across logistics segments. However, this was not the norm—names like Matson (-18.71%), Evergreen (-9.71%), Yang Ming (-9.59%), and COSCO (-9.66%) suffered some of the steepest losses, pointing to investor concern around rising costs, uncertain trade demand, and operational inefficiencies caused by global disruptions.

Geopolitically, shipping markets were pressured by persistent conflict in the Red Sea, which continued to reroute major services and increase voyage distances, pushing up fuel consumption and tightening vessel availability.

At the same time,US President Donald Trump’stariff policies, along with broader fears of a reignited U.S.–China trade war, cast a shadow over east-west container flows. European sentiment was also weighed down by speculation around reciprocal tariffs between Europe and US. These trade frictions reignited concerns over global demand fragmentation and made logistics planning increasingly complex for carriers and investors alike.

Despite this backdrop, select companies managed to hold steady thanks to charter coverage, LNG/car carrier exposure, or regional dominance in less-disrupted trade lanes. The divergence in performance suggests that while global uncertainties are here to stay, operators with agility, strong cash positions, or niche market strength may continue to weather the storm better than others.

As we move into May, markets will likely remain reactive to shifting tariff rhetoric, geopolitical flashpoints, and early indicators from Asia’s export season, keeping the shipping sector at the intersection of global trade and political volatility.

![]()

The post Shipping Stock Breakdown: April Performance Amid Global Trade Tensions appeared first on Container News.

Content Original Link:

" target="_blank">

?")