Container rates surging as shippers rush ahead of deadlines

Transpacific container rates to the West Coast doubled last week on June 1st GRIs to US$5,488/FEU, with the latest daily rates above US$6,000/FEU as shippers start peak season early and frontload goods ahead of tariff pause expirations in July and August.

Prices to the East Coast climbed 60% to US$ 6,410/FEU with the latest daily rates above US$ 7,000/FEU, with rates on both lanes about even with levels a year ago when Red Sea-driven capacity restraints combined with an early peak season rush ahead of the ILA port strike threat to push prices up.

Carriers are planning additional transpacific GRIs of US$1,000 – US$3,000/FEU for mid-June and again on July 1st. China’s ports are likely still working through some of the backlog of ready-to-ship goods created during the April-May lull in China-US demand.

In addition, some transpacific vessels and equipment that were shifted to other lanes in that period are still making their way back into place.

So as peak volumes for this year’s peak season combine with still-restrained capacity and port congestion at several Far East hubs in the near term, much of these June and July rate increases are likely to take.

By mid-July, though, rates could start to ease as demand decreases relative to what we’ve seen since mid-May, congestion eases and more capacity enters the lane.

US ports are making preparations, including some from lessons learned during the pandemic, to minimize congestion that could result from the surge of containers that will start arriving in the US soon.

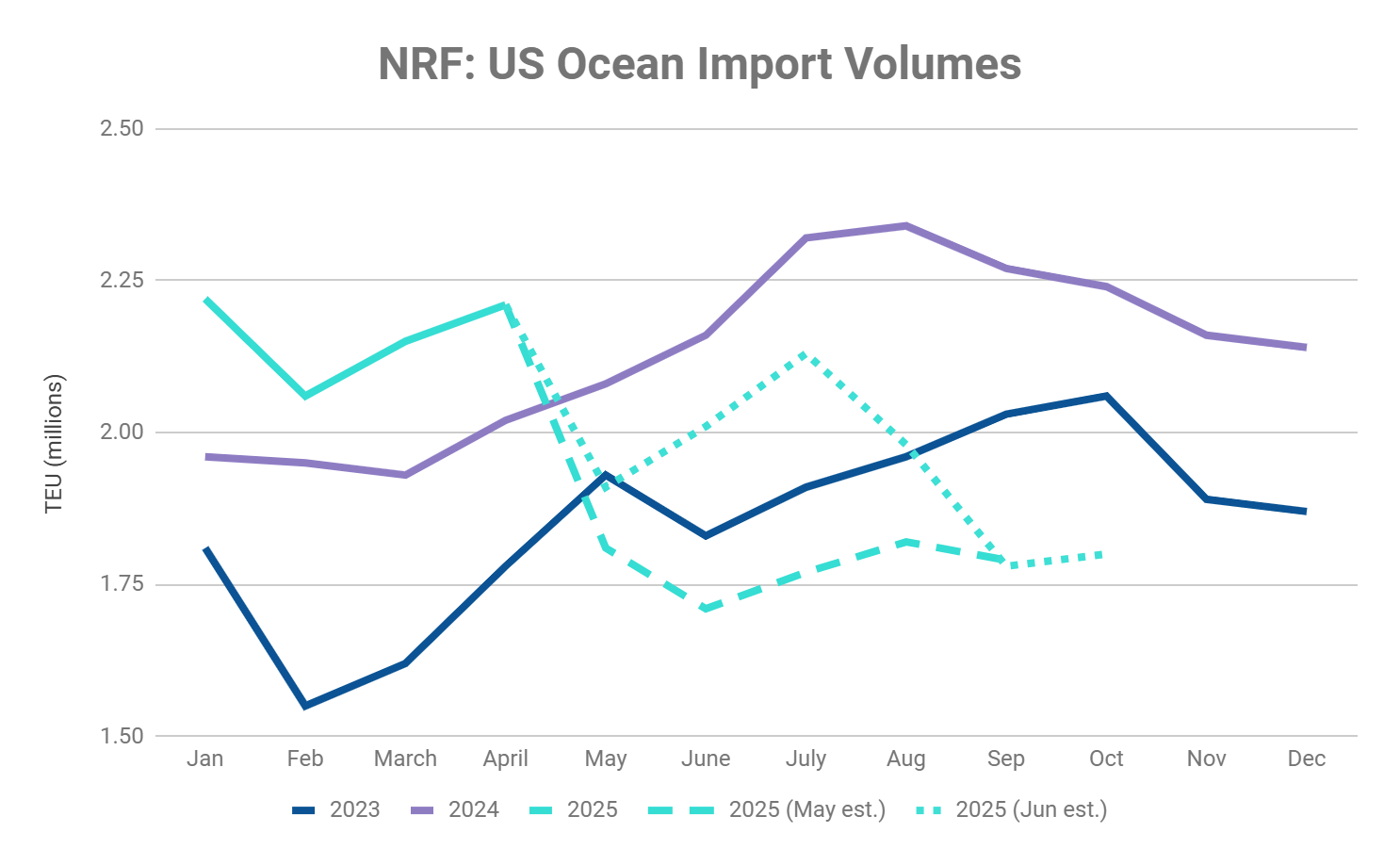

In early May, with US tariffs for China still at 145%, the National Retail Federation projected US ocean import volumes to fall significantly in May and then level off through October as high tariffs suppressed demand.

Now, the NRF – reflecting current rate behavior and GRI announcements – expects imports to rebound in June and peak in July with volumes reaching a low for the year in September post the possible tariff increases.

These projections have volumes in July – the peak of this year’s peak season – 9% lower than last year’s August peak and 4% lower than in April, this year’s strongest month to date.

These comparisons suggest that strong frontloading through April that built up inventories, and possibly some shippers decreasing shipments or pausing orders while tariffs are still at the significant minimum of 30% for China, may make this year’s tariff-deadline driven early peak season weaker than some had anticipated.

The White House continues to work toward trade agreements with a long list of major trade partners as the July and August deadlines approach.

Negotiations with China and the EU – which showed recent signs of progress following apparent steps backwards – continue even as an appeals court may decide this week whether or not to extend the stay on many of the administration’s tariffs that a US trade court voided at the end of May.

Even if talks do lead to deals and deescalation by the set deadlines, for the container market, volumes already pulled forward ahead of those dates may mean ocean demand and rates will decrease in late Q3 and into Q4 anyway.

In the meantime, surging transpacific container demand is having knock-on effects on other lanes too. Asia – Mediterranean rates spiked 32% last week to US$ 4,285/FEU with daily rates up past US$ 4,800/FEU so far this week.

And carriers are planning mid-month GRIs and PSSs for Asia-Europe and other lanes, largely due to capacity being shifted from these lanes and several others like LATAM trades to the Transpacific.

In air cargo, the plaintiff in a US court case challenging the White House’s suspension of de minimis eligibility for China – set to conclude in July – requested to expedite the trial after the court rejected a DOJ request to suspend the trial while other legal challenges to tariffs are pending.

If the court restores China’s US de minimis eligibility, some of the sharp drop in B2C e-commerce air cargo volumes could return to the market. But even with United States de minimis closed to China and keeping e-commerce volumes down, lower US tariffs on China since May 12th are driving a general cargo demand rebound on the Transpacific.

Many general air cargo shippers are now frontloading ahead of the August tariff deadline and some ocean to air shift is contributing to the volume bump too, though Freightos Air Index China-US spot rates have been level at about the US$5.25/kg mark since early May and are only about 5% lower than just before the May 2nd de minimis suspension.

China-US freighter capacity dropped by a reported 40% in mid-May compared to the year before, with some of those freighters shifted to other lanes like LATAM, the Middle East, or intra-Asia.

China-US spot rates may not have reacted to that capacity reduction since those e-commerce dedicated freighters mostly were not available to spot shippers anyway. As demand grows on the spot market post May 12th, though, rates that are nonetheless staying level may reflect freighter capacity being shifted back to the transpacific and this time being made available to general cargo shippers.”

The article was written by Judah Levine, Head of Research at Freightos

![]()

The post Container rates surging as shippers rush ahead of deadlines appeared first on Container News.

Content Original Link:

" target="_blank">