Global bunker market ends week 46 with mixed trends

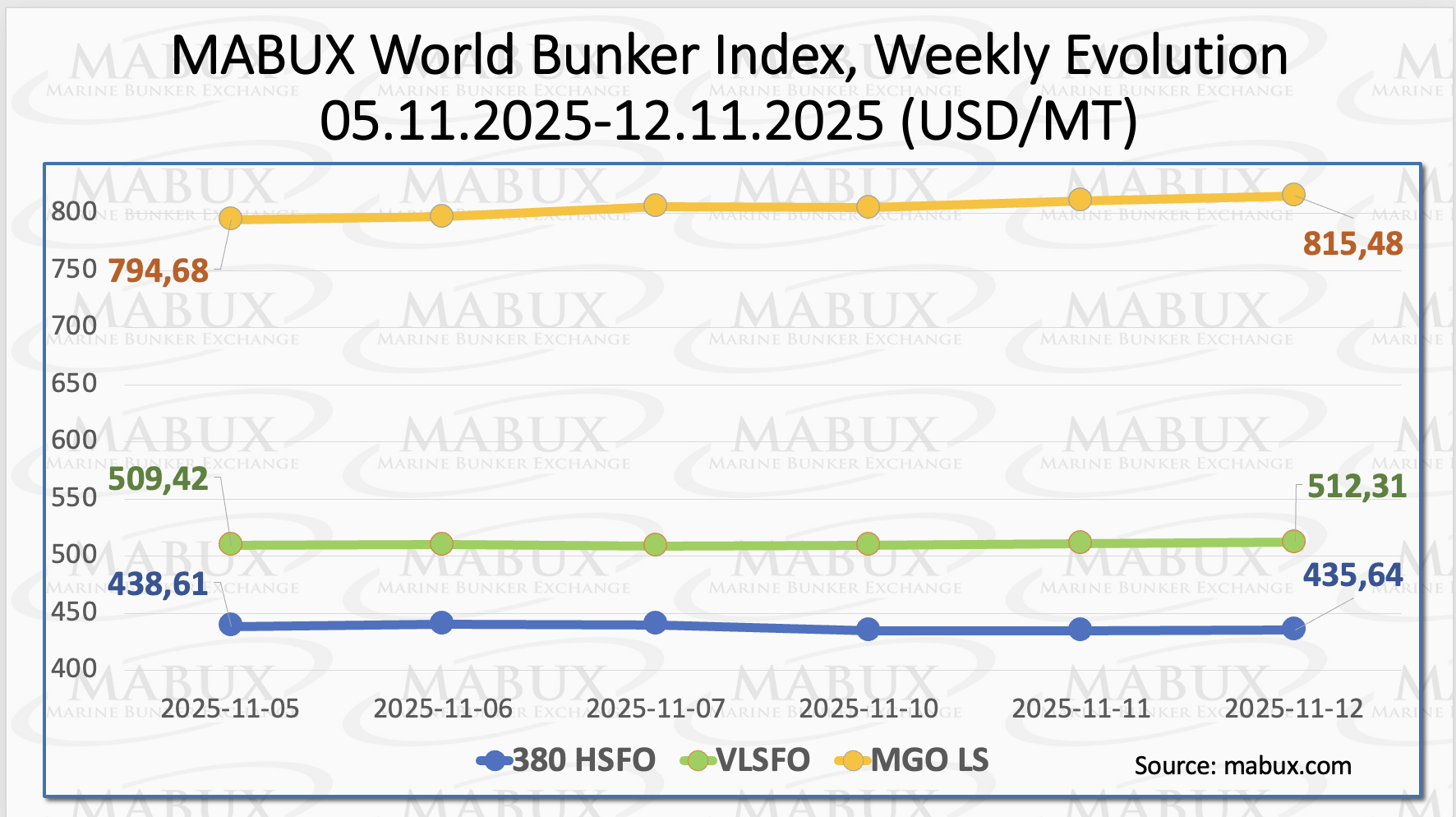

At the close of Week 46, the global bunker market continued to display mixed dynamics across major fuel grades, according to MABUX. The 380 HSFO index declined by US$2.97, dropping to US$435.64/MT.

In contrast, the VLSFO index rose by US$2.89, reaching US$512.31/MT. The MGO index also recorded a notable gain of US$20.80, climbing to US$815.48/MT, surpassing the US$800/MT threshold.

”As of the time of writing, global bunker prices continue to move in a mixed pattern, showing no distinct directional trend,” commented Sergey Ivanov, Director, MABUX.

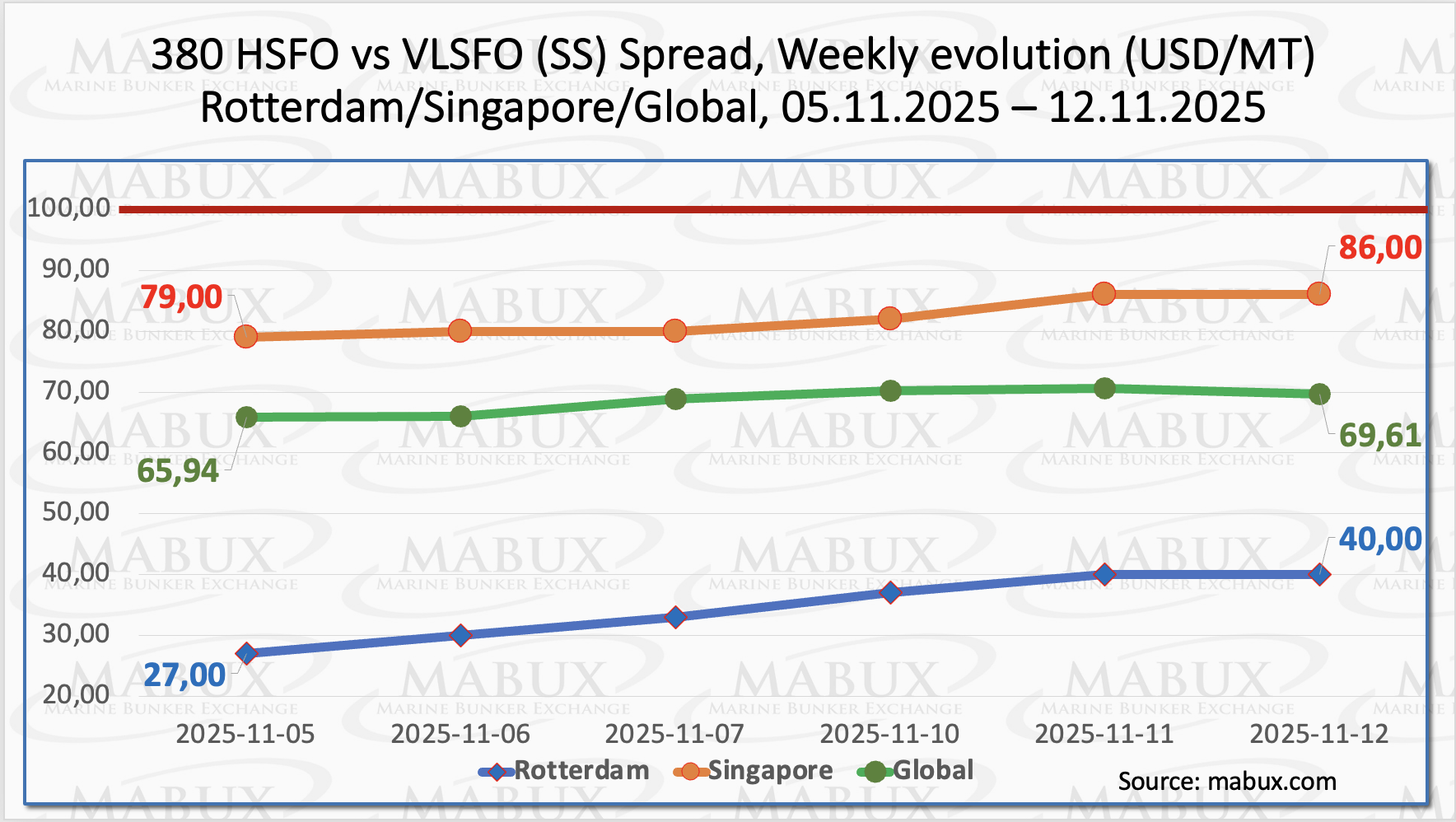

MABUX Global Scrubber Spread (SS) – the price difference between 380 HSFO and VLSFO – continued its moderate upward trend, gaining US$5.86, from $70.81/MT last week to $76.67/MT, gradually approaching the psychological mark of US$100.00 (SS Breakeven).

The weekly average value of the index also increased by US$4.39. In Rotterdam, the SS Spread also continued to rise, adding US$13.00 (US$40.00/MT), forming a stable upward movement. The port’s weekly average SS Spread grew by US$9.50. In Singapore, the price difference between 380 HSFO and VLSFO widened by US$7.00, to US$86.00/MT, exceeding the US$80.00 mark.

The weekly average value in the port also increased by US$10.00. Overall, the SS Spread trend continues to demonstrate a clear widening of the price differential between 380 HSFO and VLSFO. In the medium term, the SS Spread may again approach the US$100.00 level, which would further enhance the cost-effectiveness of using the HSFO + Scrubber combination compared with conventional VLSFO.

Global LNG markets remained broadly stable in October 2025, supported by ample supplies from the US, Qatar, and Africa, alongside easing demand from key Asian buyers. Additional volumes from US projects—including progress at Rio Grande LNG—helped sustain the global supply-demand balance, while Asian demand growth stayed muted due to mild weather and elevated inventories. LNG continued to play a vital role in stabilizing the European gas market during the third quarter of 2025: imports rose by 38% year-on-year, and regasification rates stayed near the upper end of the seasonal range.

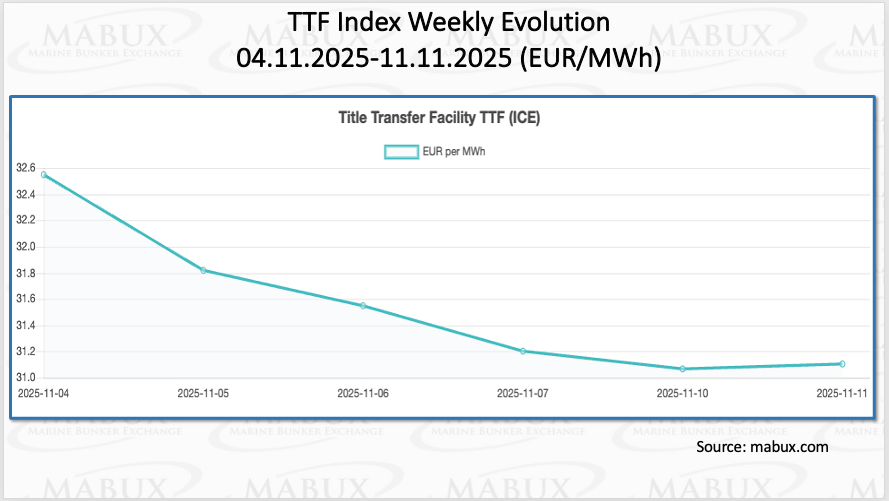

As of Nov. 11, European regional gas storage facilities were 82.39% full, down 0.63% from the previous week. With colder weather setting in, gas withdrawals have already slightly exceeded injection levels. Current storage fill remains 11.06% higher than the 71.33% recorded at the beginning of the year. The European TTF gas benchmark declined moderately during Week 46, falling by €1.449/MWh to €31.102/MWh, compared with €32.551/MWh a week earlier.

The price of LNG as bunker fuel at the port of Sines (Portugal) declined by another US$2.00 this week, to US$730/MT compared with US$732/MT the previous week. The price differential between LNG and conventional fuel remained in favor of LNG, widening to US$83 versus US$48 a week earlier, as MGO LS was quoted at US$813/MT at the port of Sines on the same day.

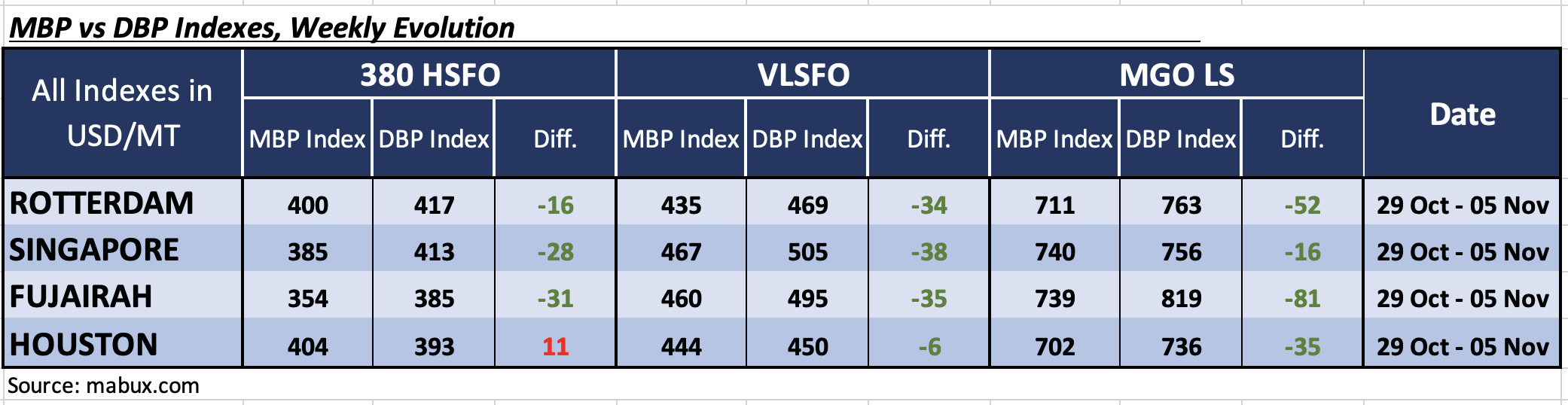

At the end of Week 46, the MABUX Market Differential Index (MDI) – the ratio of market bunker prices (MBP) to the MABUX digital bunker benchmark (DBP) – reflected the following bunker fuel price trends across the world’s largest hubs: Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: Three ports — Rotterdam, Singapore, and Fujairah — remained undervalued. The average weekly MDI values increased by 4 points in Rotterdam and 2 points in Singapore, while remaining unchanged in Fujairah. Houston was the only overvalued port in this segment, with its MDI decreasing by 2 points.

• VLSFO segment: all four ports were undercharged. The average weekly MDI undervaluation levels decreased by 5 points in Rotterdam, 9 points in Singapore, 6 points in Fujairah, and 1 point in Houston. Notably, Houston’s MDI approached a 100% correlation between MBP and DBP.

• MGO LS segment: Singapore shifted into the undervalued zone, resulting in all ports in this category being undervalued. MDI levels rose by 24 points in Rotterdam, 24 points in Singapore, and 34 points in Fujairah, but declined by 4 points in Houston. Fujairah’s MDI approached the $100.00 mark.

”By the end of the week, the overall balance of overvalued and undervalued ports continued to move toward undervaluation, most notably driven by Singapore’s shift in the MGO LS segment. We believe that the trend toward undervaluation in MDI values remains sustainable and is expected to continue in the global bunker market next week”, added Ivanov.

”We believe the global bunker market still retains growth potential. Global bunker indices may continue a moderate upward trend in the coming week”, said Sergey Ivanov, Director, MABUX.

The post Global bunker market ends week 46 with mixed trends appeared first on Container News.

Content Original Link:

" target="_blank">