Bunker prices surge in Week 10 amid Middle East tensions

Global bunker indices (MABUX) recorded a sharp increase in Week 10, driven primarily by escalating geopolitical tensions in the Middle East, which significantly impacted energy markets. According to Sergey Ivanov, Director, MABUX, the sharp escalation in the region has created immediate pressure across the global fuel complex and accelerated price volatility.

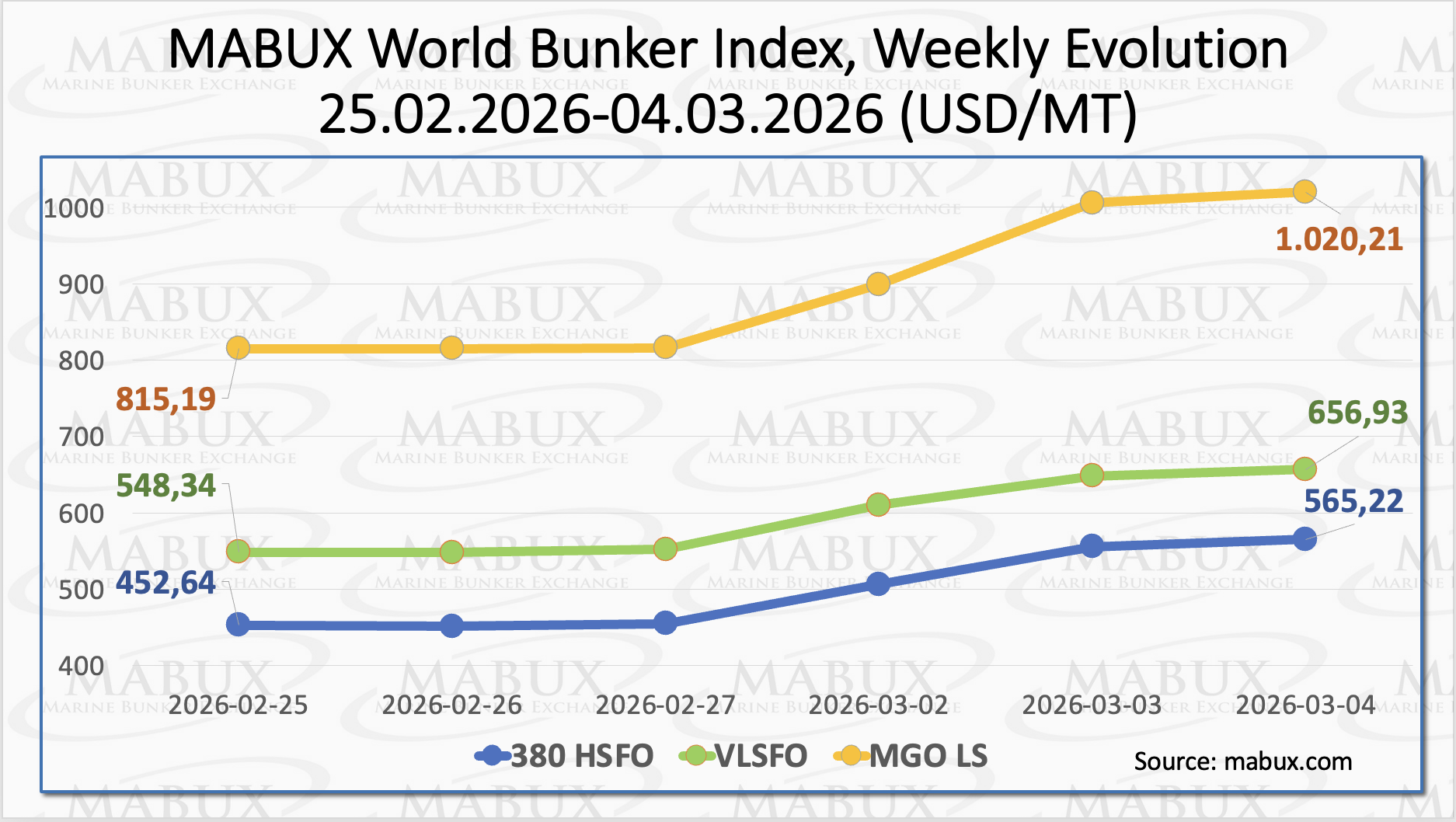

The 380 HSFO index surged by US$ 112.58, rising from US$ 452.64/MT last week to US$ 565.22/MT, comfortably exceeding the US$ 500.00 threshold. The VLSFO index also posted a substantial gain of US$ 108.59, increasing from US$ 548.34/MT to US$ 656.93/MT. The most pronounced growth was observed in the MGO LS segment, where the index climbed by US$ 205.02, from US$ 815.19/MT to US$ 1,020.21/MT. This marks the first time the MGO LS index has surpassed the US$ 1,000.00 level since October 16, 2023.

At the time of writing, however, the global bunker market has begun to show signs of a corrective downward trend following the sharp upward movement. Sergey Ivanov commented that after such an aggressive rally, short-term corrections are typical as markets reassess geopolitical risks and supply expectations.

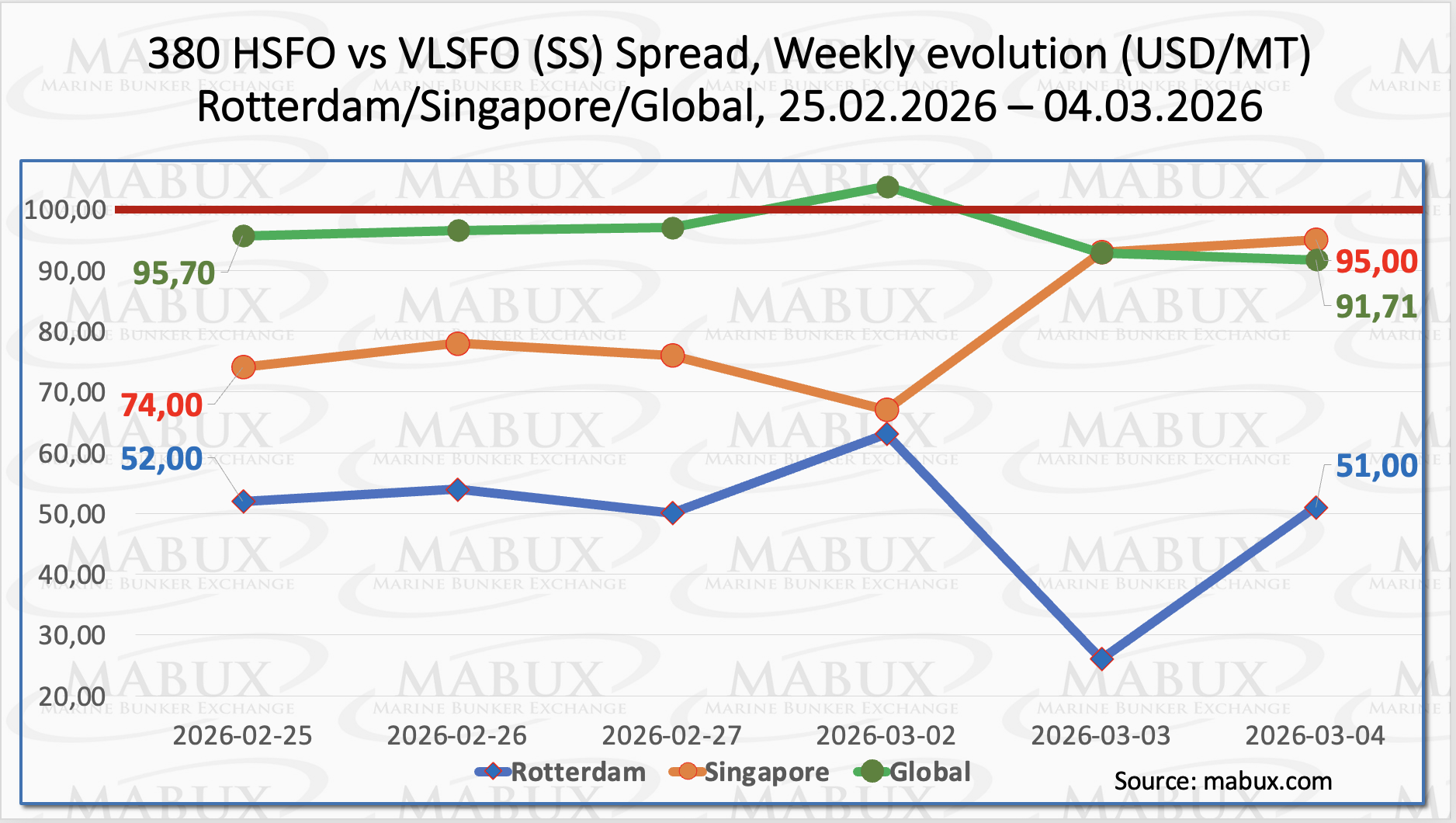

The MABUX Global Scrubber Spread (SS)—the price differential between 380 HSFO and VLSFO—narrowed slightly by US$ 3.99, declining from US$ 97.70 last week to US$ 91.71. Despite this reduction, the spread remained close to the psychological US$ 100.00 breakeven threshold for scrubber economics, while the weekly average of the index increased by US$ 4.14.

In Rotterdam, the SS Spread remained largely stable, decreasing marginally by US$ 1.00 to US$ 51.00 compared to US$ 52.00 in the previous week, while the weekly average in the port also declined by US$ 1.00. In Singapore, by contrast, the 380 HSFO/VLSFO spread continued to widen, rising by US$ 21.00 from US$ 74.00 last week to US$ 95.00, approaching the US$ 100.00 level. The weekly average spread in Singapore also increased significantly, gaining US$ 19.00.

Overall, the SS Spread ended the week with mixed dynamics across major bunkering hubs, reflecting heightened volatility in the global bunker market. Nevertheless, the spread remained below the US$ 100.00 threshold, indicating that VLSFO continues to retain stronger economic competitiveness compared to the 380 HSFO + scrubber combination. Sergey Ivanov added that geopolitical developments are currently the main factor shaping bunker price differentials between major hubs.

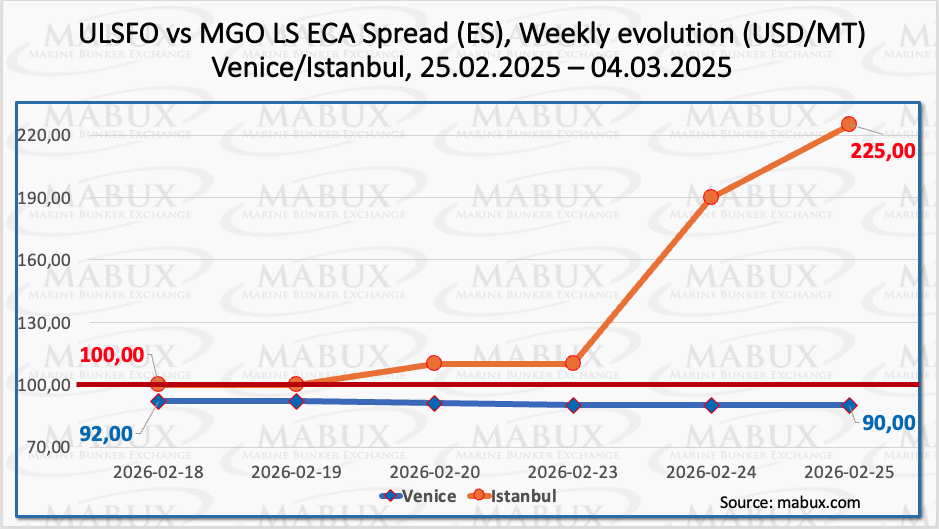

The Istanbul ECA Spread (ES) ended the week with a sharp increase, rising by US$ 125.00 from US$ 100.00 last week to US$ 225.00, while the weekly average advanced by US$ 42.50. In Venice, the ECA Spread showed only marginal changes. The index edged down slightly by US$ 2.00, from US$ 92.00 to US$ 90.00, while the weekly average recorded a modest increase of US$ 1.33.

The sharp rise in the Istanbul ES index primarily reflects a surge in diesel prices across the regional bunker market amid escalating hostilities in the Middle East, which have intensified volatility and tightened supply expectations in the distillate segment. Ivanov said that diesel markets tend to react quickly to geopolitical shocks, particularly when supply routes and refining flows become uncertain.

QatarEnergy, Qatar’s state-owned energy major, has suspended all liquefied natural gas (LNG) production following Iranian drone strikes on key facilities, effectively removing approximately 20% of global LNG supply from the market. This unprecedented disruption represents a severe supply shock with immediate and potentially structural implications for global gas markets.

Europe appears particularly exposed under these conditions. Gas inventories entering the shoulder season were already below the levels that had previously underpinned market confidence. The sudden loss of Qatari volumes significantly tightens the supply-demand balance, limiting Europe’s flexibility ahead of the next injection cycle. At the same time, Asian buyers are likely to compete aggressively for any available spot cargoes.

As of March 3, the level of gas reserves in European underground storage facilities continued to decline, falling to 29.89% of total capacity, down a further 0.70 percentage points compared to the previous week. Storage levels are now 31.57 percentage points lower than at the beginning of the year, when inventories stood at 61.46% on January 1, 2026, reflecting sustained withdrawals during the winter period and limited replenishment.

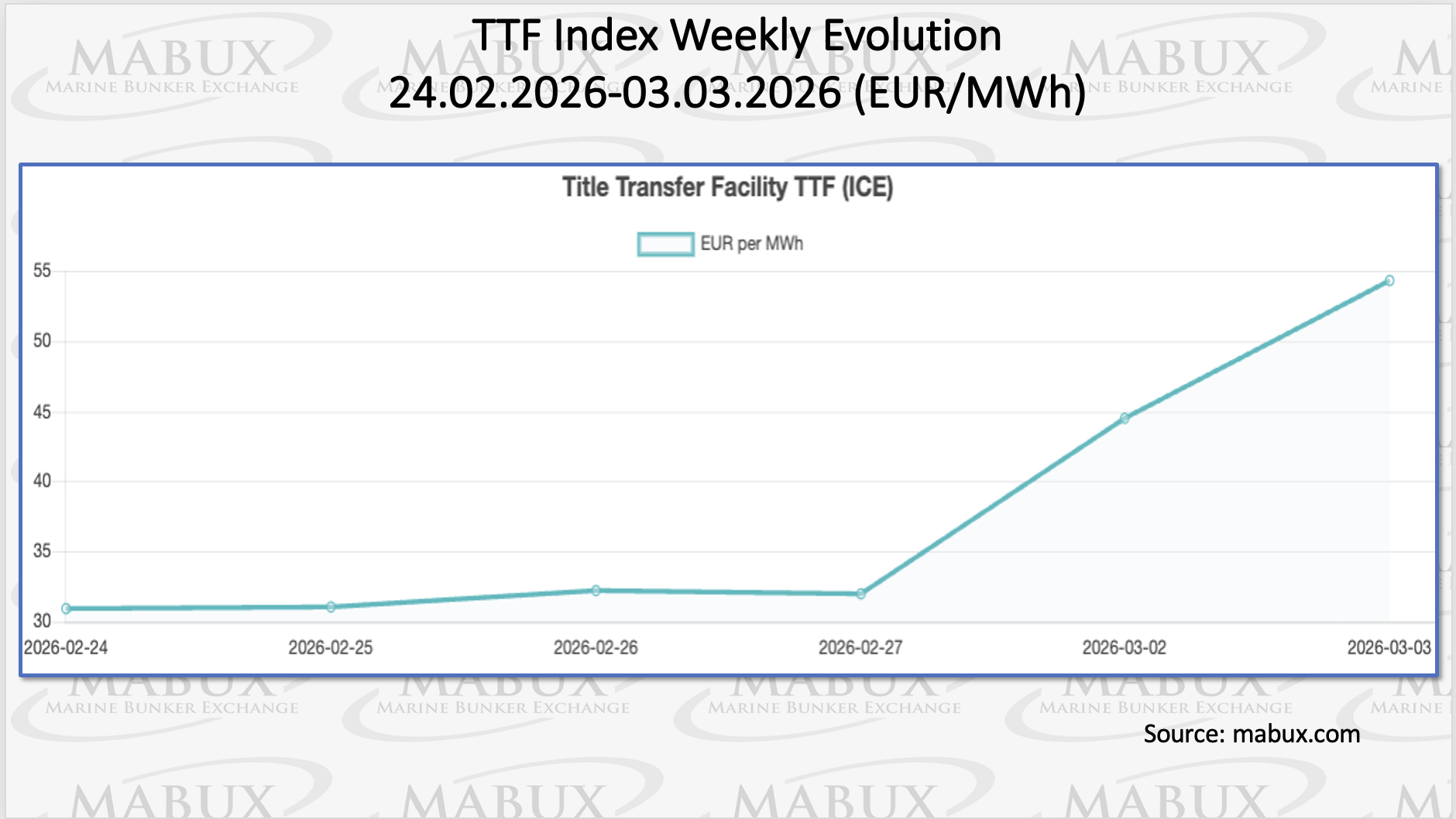

Against this backdrop, the European gas benchmark TTF recorded a sharp increase by the end of week 10, rising by EUR 23.399/MWh, from EUR 30.891/MWh in the previous week to EUR 54.290/MWh. As a result, the benchmark surpassed the EUR 50/MWh threshold, indicating a significant tightening in the regional gas market and heightened price volatility amid declining storage levels and growing geopolitical uncertainties affecting energy supply expectations.

The price of LNG as a bunker fuel at the port of Sines (Portugal) decreased marginally by US$ 1.00 week-on-week, reaching US$ 774/MT compared to US$ 775/MT the previous week. At the same time, the price differential between LNG and conventional fuel widened significantly in favor of LNG, expanding to US$ 165. As of March 2, MGO LS at the port of Sines was quoted at US$ 939/MT, reflecting a temporary upswing in bunker prices driven by escalating tensions in the Middle East.

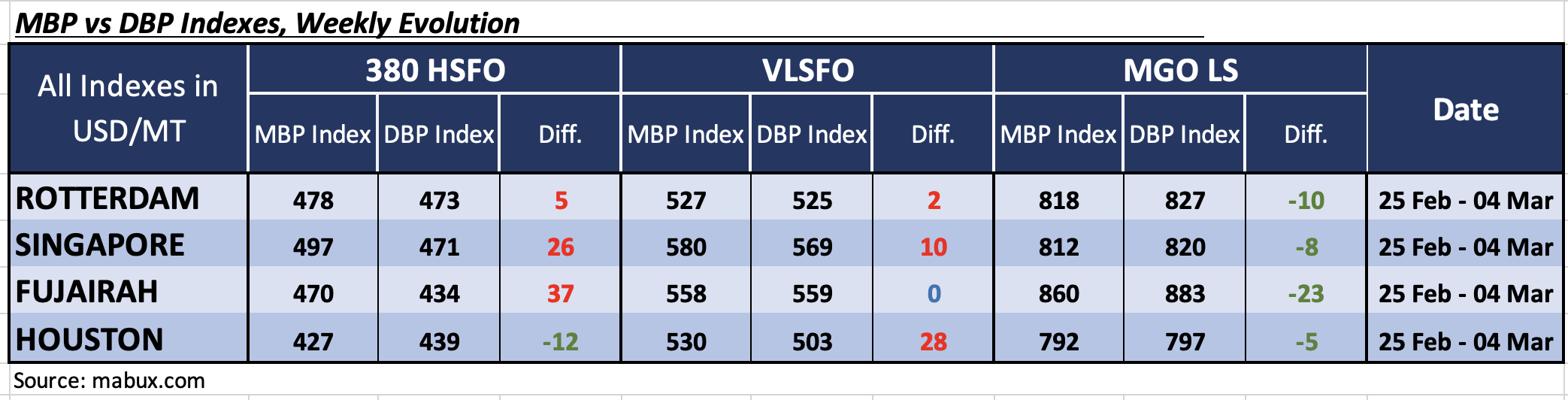

High volatility in the global bunker market has significantly altered the trends of the MABUX Market Differential Index (MDI)—which measures the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP)—across the world’s major bunkering hubs: Rotterdam, Singapore, Fujairah, and Houston.

• 380 HSFO segment: Rotterdam and Singapore moved into the overvaluation zone, joining Fujairah, with the average weekly MDI increasing by 35 points in Rotterdam, 30 points in Singapore, and 25 points in Fujairah. Houston remained the only port in the undervalued zone, with its average MDI decreasing by 33 points over the week.

• VLSFO segment: Fujairah’s MDI reached the 100% correlation level between market prices and the digital benchmark, while the other major hubs shifted into the overvalued zone. Premiums increased notably, with the MDI rising by 32 points in Rotterdam, 47 points in Singapore, and 32 points in Houston.

• MGO LS segment: all monitored ports remained in the undervalued zone, although the MDI declined further across the board. The weekly average fell by 24 points in Rotterdam, 22 points in Singapore, 4 points in Fujairah, and 54 points in Houston.

Escalating geopolitical tensions in the Middle East and the subsequent blockade of the Strait of Hormuz triggered a sharp rise in bunker prices, pushing the MDI into the overvalued zone in both the 380 HSFO and VLSFO segments. The current trend toward fuel revaluation continues to develop, and if the upward price momentum persists, the MGO LS segment may also shift into the overvalued zone in the coming week.

Overall, the prevailing market conditions suggest that fuel overvaluation may remain the dominant trend in the global bunker market in the near term. Sergey Ivanov concluded that as long as geopolitical tensions remain elevated, bunker markets are likely to stay highly volatile with continued upward pressure on global bunker indices.

The post Bunker prices surge in Week 10 amid Middle East tensions appeared first on Container News.

Content Original Link:

" target="_blank">