Grains in Q3- Can the Price Weakness Continue?

I concluded my second quarter 2025 grain and oilseed report on Barchart with the following:

The leading grains and oilseeds- corn, wheat, and soybean futures are trading at low levels compared to the 2022 highs, but they also display a long-term, multi-decade pattern of higher lows. Population growth means that production must keep pace with the fundamental equations’ ever-expanding demand side for food. Moreover, the increasing demand for biofuel puts additional upward price pressure on the agricultural products. Therefore, I continue to believe that grain and oilseed futures have limited downside and the potential for explosive upside price action. While prices could move lower as the 2025 crop year progresses, lower prices could be a buying opportunity for the coming years.

Prices did post across-the-board losses in the grain and oilseeds sector in Q3 2025 as crops were sufficient to meet the worldwide demand. However, rising production costs and low prices could be a very bullish cocktail for the coming years as producers have little incentive to ramp up output in the current environment. Moreover, the global demand continues to rise for the agricultural products that feed and increasingly power the world, as demand is a function of worldwide population trends.

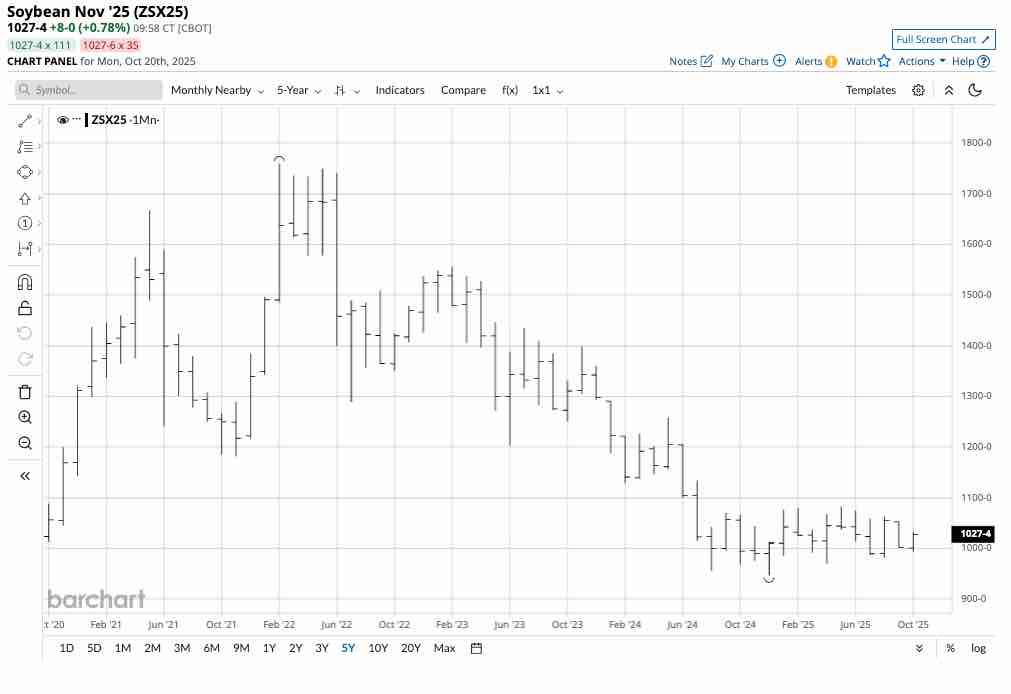

Soybean and soybean product prices fall in Q3

Nearby CBOT soybean futures declined 2.20% in Q3 2025, and were only 0.35% higher over the first nine months of 2025.

The five-year monthly chart highlights that nearby soybean futures settled at $10.0175 per bushel on September 30, 2025. In mid-October, the price was only higher at the $10.2750. While soybeans remain in a bearish trend, the price has consolidated near the low throughout 2025.

Soybean products, meal and oil, also declined in Q3. The soybean meal futures fell 2.06%, while the soybean oil dropped 6.93% over the three-month period from June 30-September 30, 2025. Soybean meal settled Q3 at $265.70 per ton on the nearby CBOT futures contract, while the oil settled at 48.87 cents per pound. Over the first nine months of 2025, the meal declined 13.66%, while the oil posted a 22.85% gain. Nearby oil futures were higher at over 51 cents per pound, while the nearby meal futures were also higher at above $283 per ton in October.

U.S. and Chinese trade policies could influence soybean prices over the coming weeks and months.

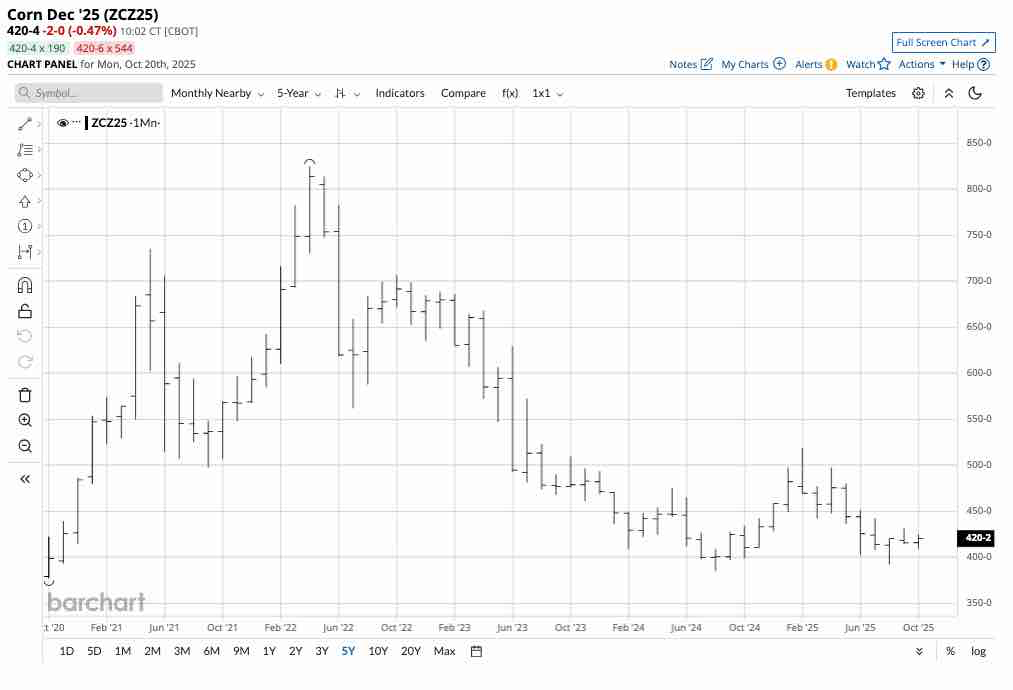

Corn adds to losses

Nearby CBOT corn futures declined 1.19% in Q3 2025, and were 9.38% lower over the first nine months of 2025.

The five-year monthly chart highlights that nearby corn futures settled at $4.1550 per bushel on September 30, 2025. In mid-October, the price was only marginally higher at the $4.2050 level. While corn futures remain in a bearish trend like soybeans, the price has also consolidated near the low throughout 2025.

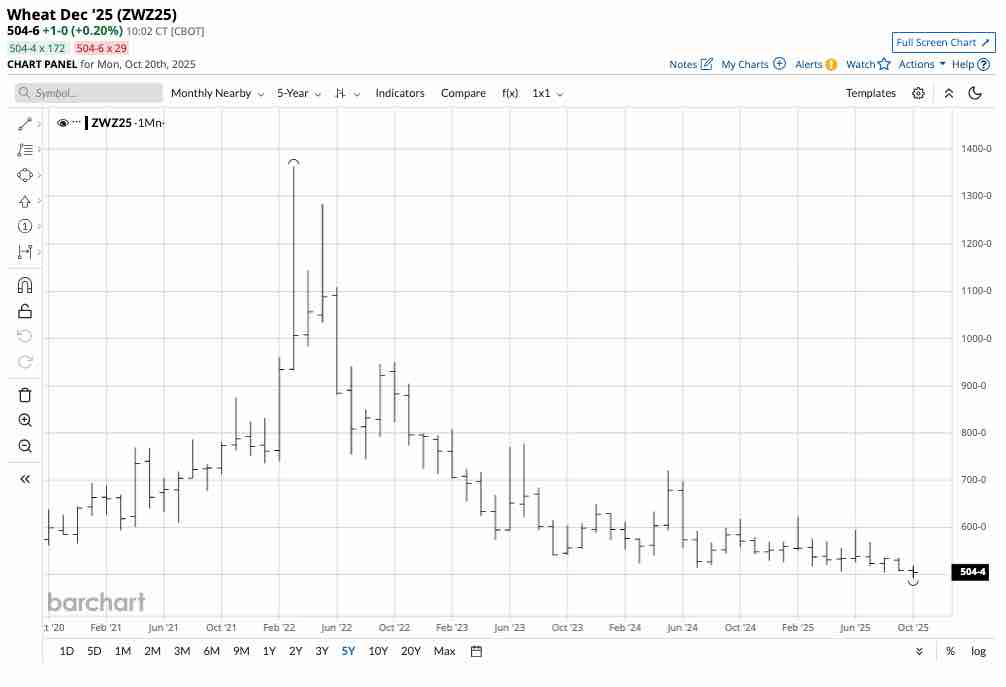

Wheat prices decline

Nearby CBOT soft red winter wheat futures declined 3.92% in Q3 2025, and were 7.89% lower over the first nine months of 2025.

The five-year monthly chart highlights that nearby soft red winter wheat futures settled at $5.0800 per bushel on September 30, 2025. In mid-October, the price was marginally lower at $5.0475 per bushel. While the CBOT wheat futures remain in a bearish trend, similar to corn and soybeans, the price has also consolidated near the low throughout 2025, but wheat fell to a lower low in early Q4.

Nearby KCBT hard red winter wheat futures declined 1.63% in Q3 2025, and were 11% lower over the first nine months of 2025. The hard red winter wheat futures settled at $4.9775 per bushel on September 30, 2025. In mid-October, the price was marginally lower at close to $4.90 per bushel. Many U.S. bread manufacturers price requirements are based on the KCBT wheat futures price. The spread between KCBT and CBOT wheat, which typically commands a premium for the KCBT wheat futures, fell to a discount in 2025, indicating weak hedging and speculative demand.

Nearby MGE spring wheat futures declined 6.67% in Q3 2025, and were 5.54% lower over the first nine months of 2025. The spring wheat futures settled at $5.6275 per bushel on September 30, 2025. In mid-October, the price was lower at the $5.50 per bushel level.

Significant declines in oats and rice futures

Nearby CBOT oat futures declined 20.49% in Q3 2025, and were 6.96% lower over the first nine months of 2025. The nearby oat futures settled at $3.0750 per bushel on September 30, 2025. In mid-October, the price was lower at under $3 per bushel.

Nearby CBOT rough rice futures declined 13.82% in Q3 2025, and were 20.39% lower over the first nine months of 2025. The nearby rough rice futures settled at $11.165 per cwt on September 30, 2025. In mid-October, the price was lower at $10.59 per cwt.

The outlook for Q4 and beyond- A lack of fundamental USDA data

Grain and oilseed prices continue to languish and remain in mostly bearish trends in Q4 2025. The 2025 crop was sufficient to meet the global food and biofuel requirements.

In early Q4, the market suffers from a lack of fundamental transparency as the U.S. government shutdown has caused the USDA to suspend its monthly World Agricultural Supply and Demand Estimates Report, which is the fundamental gold standard for the sector.

While the lack of USDA data presents some roadblocks, the price action in the grain and oilseed markets tells us all we need to know. Supplies are robust to meet the worldwide demand, and prices remain near multiyear lows. However, each year is a new adventure in the agricultural sectors, and commodity cyclicality suggests that prices are at or near levels that will discourage production, reduce inventories, and increase demand, leading to higher prices over the coming months and years. Moreover, the weather in the critical growing regions and developments in worldwide trade could cause sudden price volatility. At the current levels, prices have limited downside potential, while the upside could be substantial. I favor long positions in the sector, leaving plenty of room to add on further declines over the coming months. The 2026 crop year and supply uncertainty are just around the corner in early 2026, which could ignite price recoveries.

On the date of publication, Andrew Hecht did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

Content Original Link:

" target="_blank">